Mortgage Blog

Your Complete Guide to a CMHC Insured Construction Mortgage in Burlington

July 9, 2026 | Posted by: Matt Shepherd

Understanding the High-Ratio Construction Mortgage

Building your dream home in Burlington, ON is an exciting journey, but financing the build requires the right strategy. An Insured Construction Mortgage, often referred to as a High-Ratio Construction Mortgage, is designed for borrowers who want to build a new home but have less than a 20% down payment. By securing a cmhc insured construction mortgage, you can access the funds needed to complete your project while benefiting from competitive interest rates.

If you are navigating the complexities of construction to permanent mortgage options, understanding the nuances of Insured Construction is crucial. At Jason Woods Mortgages, we specialize in helping Burlington residents structure these unique loans. We are also experts at providing second opinions on insured construction mortgages, ensuring you get the best terms possible for your specific build.

- Requires as little as 5% down payment for the first $500,000.

- Backed by the Canada Mortgage and Housing Corporation (CMHC).

- Funds are released in stages as the build progresses.

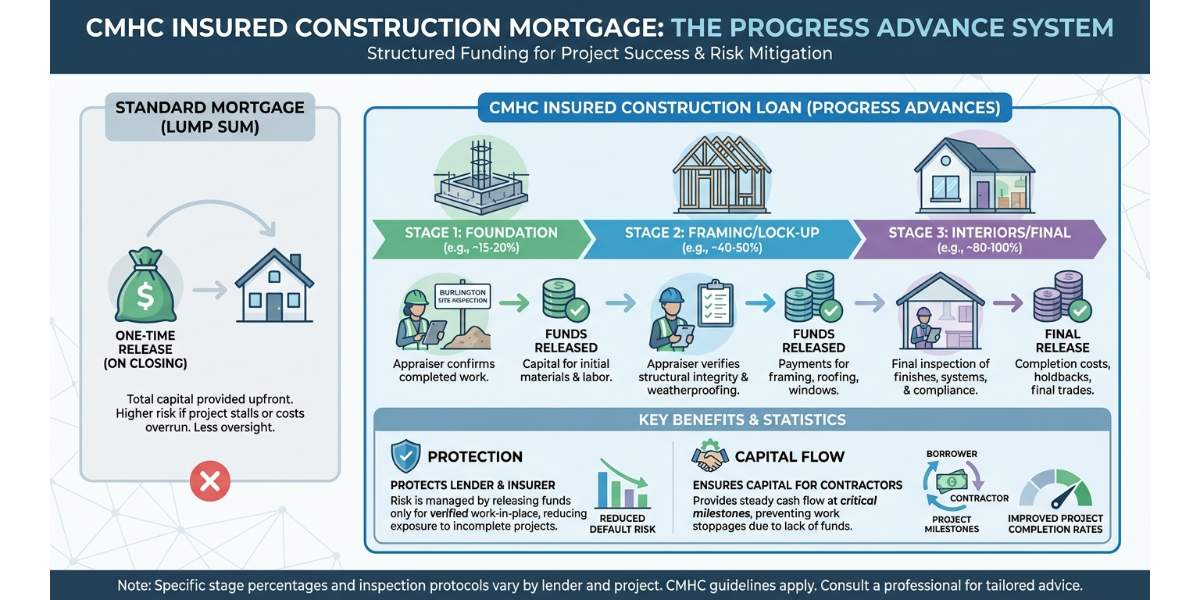

How the Progress Advance System Works

A key feature of a cmhc insured construction mortgage is the progress advance system. Unlike a standard mortgage where you receive a lump sum on closing day, an insured construction loan releases funds in scheduled stages. This protects the lender and the insurer while ensuring you have the capital required to pay your contractors at critical milestones.

Typically, a progress advance involves several stages of inspection. An appraiser visits the Burlington site to confirm the work is completed before the next portion of your mortgage is released. If you are ever unsure about your current lender's draw schedule, remember that we are experts at providing second opinions on insured construction mortgages to keep your project on track.

Here are the standard draw stages you can expect:

- First Advance: Foundation is poured and completed.

- Second Advance: The home is completely framed, and the roof is on (lock-up stage).

- Third Advance: Drywall is installed and taped, and plumbing and electrical are roughed in.

- Final Advance: The home is 100% complete and ready for occupancy.

For more information on financing your build, explore our mortgage services to see how we can assist you from the ground up.

| Construction Stage | Completion Percentage | Typical Advance Amount | Appraisal Required |

|---|---|---|---|

| 1. Excavation & Foundation | 15% | 15% of total loan | Yes |

| 2. Framing & Roof (Lock-up) | 40% | 25% of total loan | Yes |

| 3. Drywall & Rough-ins | 65% | 25% of total loan | Yes |

| 4. Completion & Occupancy | 100% | 35% of total loan | Yes |

Why Choose Jason Woods for Your CMHC Insured Construction Mortgage

Securing a high-ratio construction mortgage requires a broker who understands the local Burlington market and the strict guidelines set by CMHC. As your dedicated principal broker, Jason Woods will guide you through the entire process, from your initial mortgage pre-approval to the final progress advance.

We know that building a home can be stressful, which is why having an expert in your corner is invaluable. If you have already started the process but feel uncertain about your approval terms, reach out to us. We are experts at providing second opinions on insured construction mortgages, giving you the peace of mind that your financing is solid.

Whether you are considering a construction to permanent mortgage or simply need advice on the best path forward, our team is ready to help you build a better mortgage.

Q1: What is a CMHC insured construction mortgage?

It is a high-ratio loan backed by the Canada Mortgage and Housing Corporation, allowing borrowers to build a home with less than a 20% down payment.

Q2: How does a progress advance work?

Funds are released in stages as your home is being built. An appraiser verifies the completion of each stage before the lender releases the next portion of the funds to pay your builders.

Q3: Can I get a second opinion on my insured construction mortgage?

Absolutely. We are experts at providing second opinions on insured construction mortgages to ensure you have the best rates and draw schedules for your specific project.

Q4: What is the difference between a high-ratio construction mortgage and a construction to permanent mortgage?

A high-ratio construction mortgage specifically refers to the insured funding during the build phase for those with smaller down payments, while a construction to permanent mortgage is a structure where the initial construction loan automatically converts into a standard permanent mortgage once the build is complete.

Q5: Do you serve areas outside of Burlington, ON?

Yes, Jason Woods proudly serves Burlington, Hamilton, Oakville, Toronto, and surrounding areas for all residential and construction mortgage needs.

Contact Jason Woods Today at 289-925-9599 for Your Free Second Opinion