Mortgage Blog

Understanding the Open Mortgage in Canada: Your Guide to Ultimate Flexibility

July 7, 2026 | Posted by: Matt Shepherd

What is an Open-Term Mortgage and How Does It Work?

When navigating the housing market in Burlington, ON and surrounding areas like Oakville and Hamilton, having the right financing strategy is crucial. An open mortgage, also widely known as an open-term mortgage, provides unparalleled flexibility for homeowners. Unlike a traditional closed mortgage, an open mortgage allows you to pay off your principal balance in part or in full at any time without facing hefty prepayment penalties.

For many Canadians, a primary focus when searching for the best open mortgage Canada has to offer means seeking out financial freedom. Whether you are expecting a large inheritance, planning to sell your property shortly, or simply want the peace of mind to pay down your debt aggressively, an open mortgage could be your ideal solution. However, this flexibility often comes with slightly higher interest rates compared to closed terms. That is exactly why working with a local expert is vital. At Jason Woods Mortgages (TLC Mortgage Group | Lic. 12988), we are experts at providing second opinions on open mortgages to ensure you are getting the rate and terms you deserve.

- Total Flexibility: Make lump-sum payments whenever you choose.

- No Prepayment Penalties: Sell or refinance without breaking fees.

- Short-Term Solutions: Ideal for transitional periods between homes.

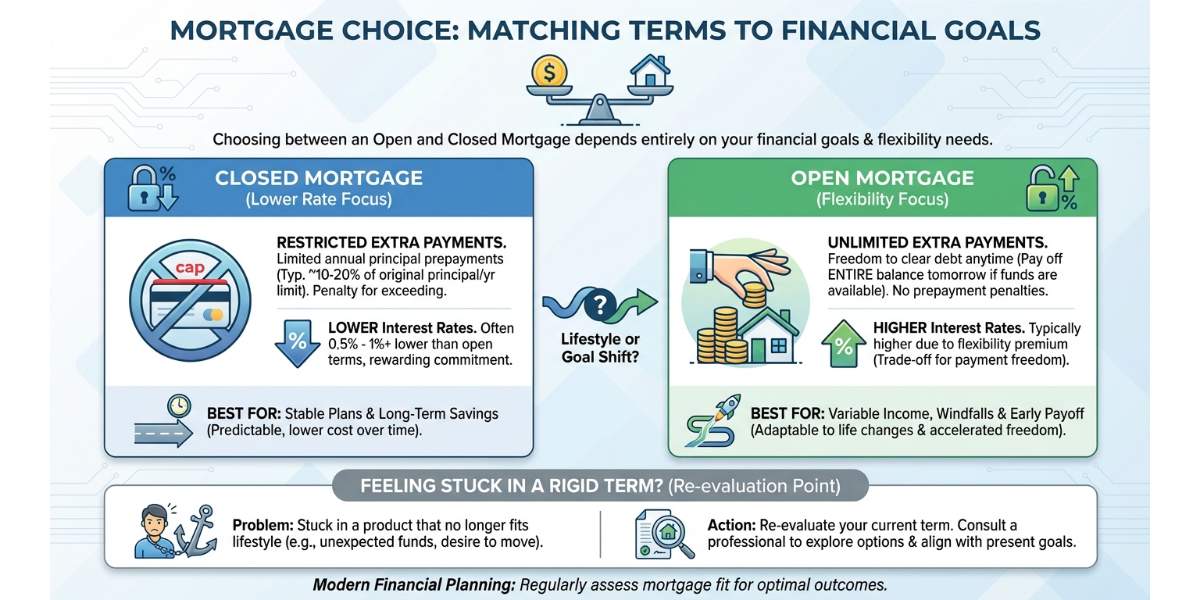

Open Mortgage vs. Closed Mortgage: Making the Right Choice

Choosing between an open mortgage and a closed mortgage depends entirely on your financial goals. A closed mortgage restricts how much extra you can pay toward your principal each year, but it rewards you with lower interest rates. On the other hand, an open-term mortgage gives you the freedom to clear your debt tomorrow if you have the funds available.

Sometimes, homeowners find themselves stuck in a product that no longer fits their lifestyle. If you are currently locked into a rigid term and looking for more flexibility, it might be time to explore a switch and transfer mortgage. Switching lenders or mortgage types can help you secure an open mortgage structure that aligns with your current needs. Whether you are in Burlington, Toronto, or anywhere in between, Jason Woods can guide you through the transition smoothly.

Remember, we specialize in offering a free, no-obligation second opinion on your current mortgage setup. If you are questioning whether an open mortgage is right for you, let us review your files and provide expert, localized advice tailored to your unique situation.

| Feature | Open Mortgage | Closed Mortgage |

|---|---|---|

| Prepayment Penalties | None | Yes (typically 3 months interest or IRD) |

| Interest Rates | Generally Higher | Generally Lower |

| Flexibility | Maximum (Pay off anytime) | Limited (Annual prepayment privileges apply) |

| Ideal For | Short-term planning, expected windfalls, frequent movers | Long-term stability, budget predictability |

Why Get a Second Opinion on Your Open Mortgage in Burlington?

The Canadian mortgage landscape is constantly shifting. Even if you already have an open mortgage, are you certain you have the best possible rate? As your dedicated Burlington mortgage broker, Jason Woods has access to over 40 lenders. This means we can shop the market to ensure your open mortgage Canada terms are truly competitive and working in your favor.

Getting a second opinion is fast, simple, and secure. We evaluate your current financial standing, your future real estate goals, and your existing mortgage contract. If a better option exists, perhaps transitioning via a switch and transfer mortgage, we will find it for you. Do not leave your hard-earned money on the table; let an expert do the mortgage shopping for you so you can focus on enjoying your home.

Q1: What is the main advantage of an open mortgage in Canada?

The primary advantage is flexibility. You can pay off your entire mortgage balance at any time without incurring any prepayment penalties, making it perfect for those expecting a windfall or planning to sell soon.

Q2: Can I switch from a closed mortgage to an open mortgage?

Yes, you can. This is often done at renewal time to avoid fees, or through a switch and transfer mortgage if the benefits of breaking your current closed term outweigh the penalty costs.

Q3: Why are interest rates higher on open-term mortgages?

Lenders charge a premium for the flexibility they offer. Because they cannot guarantee how much interest they will earn over a set period, the slightly higher rate compensates for that uncertainty.

Q4: Is an open mortgage a good idea for first-time home buyers?

It depends on the financial situation of the buyer. While most first-time buyers opt for the lower rates of a closed mortgage, an open mortgage might make sense if they plan to flip the property or expect a significant increase in income shortly after purchase.

Q5: How can Jason Woods help me with my open mortgage?

We are experts at providing second opinions on open mortgages. By leveraging access to over 40 lenders, Jason Woods can review your current terms and ensure you are getting the most competitive rate and structure available in Burlington and surrounding areas.