Mortgage Blog

Understanding the Closed Mortgage: Your Guide to Secure Home Financing in Burlington

July 2, 2026 | Posted by: Matt Shepherd

What is a Closed Mortgage and Why Choose One?

When navigating the real estate market in Burlington, ON, finding the right financing is crucial. A closed mortgage, also known as a closed-term mortgage, is one of the most popular choices for homebuyers seeking stability. But what exactly does it mean? Essentially, a closed mortgage requires you to commit to a specific interest rate and payment schedule for a set term. In exchange for this commitment, lenders typically offer lower interest rates compared to an open-mortgage.

For many families, knowing exactly what their monthly payments will be brings incredible peace of mind. However, breaking this type of mortgage before the term ends usually incurs a prepayment penalty. That is why getting the right advice upfront is so important. At the office of Jason Woods, we are experts at providing second opinions on closed mortgages to ensure you are getting the best possible terms for your financial situation.

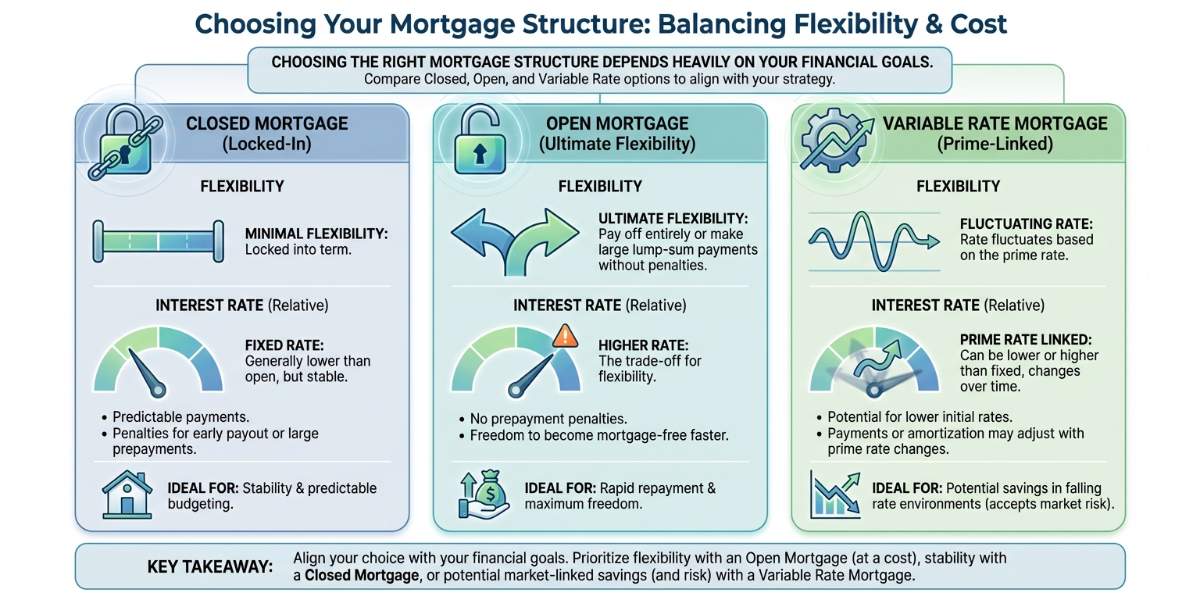

Comparing Closed, Open, and Variable Rate Mortgages

Choosing the right mortgage structure depends heavily on your financial goals. While a closed mortgage locks you in, an open-mortgage provides the ultimate flexibility, allowing you to pay off your mortgage entirely or make large lump-sum payments without penalties. The trade-off is that open mortgages generally come with higher interest rates.

Another excellent option to consider is a variable-rate-mortgage-prime-linked. With a variable rate, your interest rate fluctuates based on the prime lending rate. If rates drop, more of your payment goes toward the principal. Here is a quick breakdown to help you decide:

- Closed-Term Mortgage: Best for those who want predictable payments and lower interest rates.

- Open Mortgage: Ideal if you plan to sell your home soon or expect a large financial windfall.

- Variable-Rate Prime Linked: A great choice if you have a flexible budget and want to take advantage of potentially falling interest rates.

As your dedicated Burlington mortgage broker, I can help you weigh these options and find the perfect fit for your lifestyle.

| Mortgage Type | Interest Rate Typically | Prepayment Flexibility | Best Suited For |

|---|---|---|---|

| Closed Mortgage | Lowest | Limited (usually 10% to 20% annually) | Long-term stability and strict budgets |

| Open Mortgage | Highest | Unlimited (no penalties) | Short-term ownership or expected lump sums |

| Variable-Rate (Prime-Linked) | Variable (fluctuates) | Moderate (often 3 months interest penalty) | Borrowers comfortable with market fluctuations |

Expert Second Opinions on Your Closed-Term Mortgage

Are you currently locked into a closed-term mortgage and wondering if you have better options? We are experts at providing second opinions on closed mortgages. Even with prepayment penalties, refinancing to a lower rate or accessing home equity for debt consolidation can sometimes save you thousands of dollars in the long run.

Working with an experienced mortgage broker in Burlington, ON, ensures you have access to over 40 lenders, not just one bank. My goal is to make your financing fast, simple, and secure. Whether you are a first-time homebuyer or looking for mortgage refinancing, professional advice is the best place to start.

Compliance Notice: Jason Woods is the Principal Broker at TLC Mortgage Group (Lic. 12988). All mortgage approvals are subject to qualification and lender criteria.

Q1: What is a closed mortgage?

A closed mortgage, also known as a closed-term mortgage, is a home loan where the interest rate and term are fixed. You cannot pay off the full balance before the term ends without incurring a prepayment penalty.

Q2: Can I make extra payments on a closed mortgage?

Yes, most lenders offer prepayment privileges. This typically allows you to pay 10 to 20 percent of the original principal balance each year without a penalty.

Q3: How does a closed mortgage differ from an open-mortgage?

An open-mortgage allows you to pay off your entire loan at any time without penalties, but it usually comes with a higher interest rate compared to the more restrictive closed mortgage.

Q4: Should I choose a closed mortgage or a variable-rate-mortgage-prime-linked?

It depends on your risk tolerance. A closed mortgage offers fixed, predictable payments, while a variable-rate-mortgage-prime-linked fluctuates with the market, potentially saving you money if prime rates drop.

Q5: Do you offer second opinions on existing closed mortgages?

Absolutely. We are experts at providing second opinions on closed mortgages and can help you determine if breaking your current term to refinance makes financial sense.

Ready to Review Your Mortgage Options?

Contact Jason Woods today to get the mortgage you deserve.

Email Jason Woods NowOr call directly at 289-925-9599