Mortgage Blog

Your Guide to a Portable Mortgage in Canada: Switch and Transfer Mortgages Explained

July 1, 2026 | Posted by: Matt Shepherd

Understanding Mortgage Porting and Assumption Transfers in Burlington

If you are planning to move to a new home in Burlington, ON, or the surrounding areas like Hamilton and Oakville, you might be wondering what happens to your current mortgage. A portable mortgage, also commonly known as a switch and transfer mortgage, allows you to take your existing interest rate and terms with you to your new property. This can be a massive money saver, especially if your current rate is lower than today's market offerings.

As an experienced mortgage broker in Burlington, Jason Woods and the TLC Mortgage Group specialize in helping homeowners navigate the complexities of a portable mortgage in Canada. Whether you are exploring mortgage porting or looking into assumption transfers, getting a professional second opinion is crucial. We are experts at providing second opinions on switch and transfer mortgages to ensure you are not leaving money on the table.

- Mortgage Porting: Transferring your current mortgage rate and balance to a new property.

- Assumption Transfers: Allowing a buyer to take over your existing mortgage terms when they purchase your home.

Before you break your current term and pay hefty penalties, it is always wise to explore your transfer options. If you need to access additional equity during your move, you might also want to look into mortgage refinancing.

How Does a Switch and Transfer Mortgage Work?

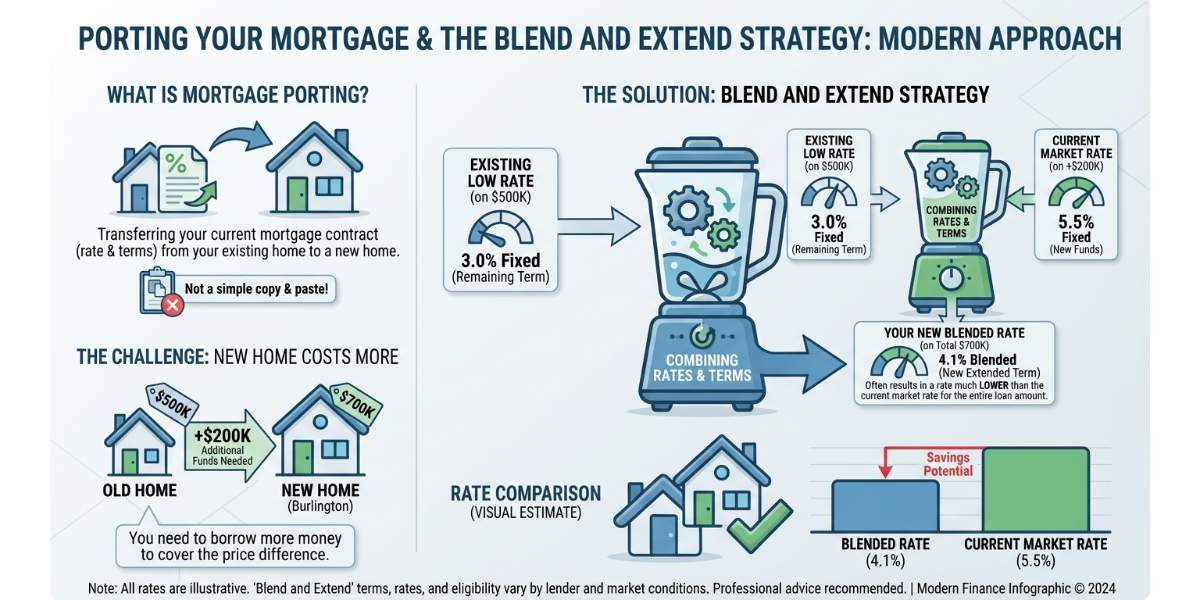

Porting your mortgage is essentially picking up your current mortgage contract and dropping it onto your new home. However, it is not always a simple copy and paste. If your new home in Burlington costs more than your previous one, you will need to borrow additional funds. This is where a 'blend and extend' strategy comes into play.

With a blended rate, your lender will combine your existing low mortgage rate with the current market rate for the new funds you need. This often results in a much better overall rate than starting from scratch. Here are a few things to keep in mind when considering a portable mortgage:

- Timing is everything: Most lenders require you to close on your new home within 30 to 120 days of selling your old one to keep your portable mortgage status.

- Qualification still applies: Even though you are keeping your current mortgage, the lender will still require a mortgage pre-approval for the new property to ensure you meet current lending guidelines.

- Not all mortgages are portable: Variable rate mortgages often cannot be ported directly without converting them to a fixed rate first.

To see how a new loan amount might affect your monthly budget, try using our mortgage calculators. If you are unsure whether your current lender is offering you the best blended rate, reach out to Jason Woods for a free second opinion.

| Feature | Breaking Mortgage | Portable Mortgage (Porting) | Assumption Transfer |

|---|---|---|---|

| Interest Rate | Current market rate | Keep existing rate (or blended rate) | Buyer keeps seller's rate |

| Penalties | High prepayment penalties | Usually none (if ported within timeframe) | None for the seller |

| Flexibility | High (choose any lender) | Low (must stay with current lender) | Low (buyer must qualify with current lender) |

| Best For | When current rates are lower | When your existing rate is lower | Sellers wanting to offer incentives |

Why Get a Second Opinion on Your Portable Mortgage in Canada?

When you ask your current bank about a switch and transfer mortgage, they will only offer you their specific products. This limits your options. As an independent mortgage broker serving Burlington, Hamilton, Oakville, and Toronto, Jason Woods has access to over 40 different lenders. We know mortgages, and we know how to find the right fit for your unique situation.

Getting a second opinion on your portable mortgage can uncover hidden fees, highlight better blending options, or even reveal that breaking your mortgage and switching to a new lender is actually the cheaper route. Sometimes, utilizing mortgage refinancing makes more financial sense than porting, depending on the penalties and your need for debt consolidation.

Here is why Burlington homeowners choose TLC Mortgage Group for their switch and transfer needs:

- Expertise: We specialize in complex transactions like assumption transfers and mortgage porting.

- Speed: We offer fast mortgage pre-approvals because we know speed matters when securing your next home.

- Unbiased Advice: We work for you, not the banks. Our goal is to build you a better mortgage.

Do not let the stress of moving cloud your financial judgment. Let us review your portable mortgage offer today.

Q1: What is a portable mortgage in Canada?

A portable mortgage allows you to transfer your existing mortgage rate, balance, and terms to a new property when you move, helping you avoid prepayment penalties and keep a favorable interest rate.

Q2: Can I port my mortgage if the new house is more expensive?

Yes, you can. If you need more money to purchase a more expensive home, your lender will typically offer a blended rate. This combines your current lower interest rate with the current market rate for the additional funds required.

Q3: What is the difference between mortgage porting and an assumption transfer?

Mortgage porting is when you take your mortgage with you to a new property. An assumption transfer is when the person buying your current home takes over your existing mortgage and its terms.

Q4: How long do I have to port my mortgage after selling my home?

Most Canadian lenders provide a window of 30 to 120 days to complete the purchase of your new home and successfully port your switch and transfer mortgage.

Q5: Why should I get a second opinion on a switch and transfer mortgage?

A second opinion from a Burlington mortgage broker like Jason Woods ensures you are getting the best possible blended rate and terms. We can compare your current lender's offer against over 40 other lenders to see if porting is truly your most cost-effective option.

Get Your Free Second Opinion on Your Portable Mortgage Today