Mortgage Blog

Your Complete Guide to the Cash-Back Mortgage in Burlington, ON

April 28, 2026 | Posted by: Matt Shepherd

Understanding the Cash Back Mortgage Canada Landscape

If you are looking to purchase a home in Burlington or the surrounding areas, finding the right financing is a critical step. A Cash-Back Mortgage, also known as a Cashback Mortgage, is a unique financing solution that provides you with a lump sum of cash up front when your mortgage closes. This type of loan is becoming increasingly popular in the cash back mortgage Canada market, especially for buyers who need extra funds for closing costs, moving expenses, or immediate renovations.

As an experienced Principal Broker in Burlington, ON, Jason Woods and the team at TLC Mortgage Group understand that every homebuyer has unique needs. We are experts at providing second opinions on cash-back mortgages. We evaluate your financial situation to determine if this product aligns with your long-term goals. Whether you are considering a closed-mortgage for a lower fixed rate or an open-mortgage for maximum prepayment flexibility, understanding the terms is crucial.

- Immediate Funds: Receive a percentage of your mortgage amount in cash at closing.

- Flexibility: Use the funds for debt consolidation, buying furniture, or covering land transfer taxes.

- Expert Second Opinions: We review existing offers to ensure you are getting the best terms possible.

How Cashback Mortgages Compare to Open and Closed Mortgages

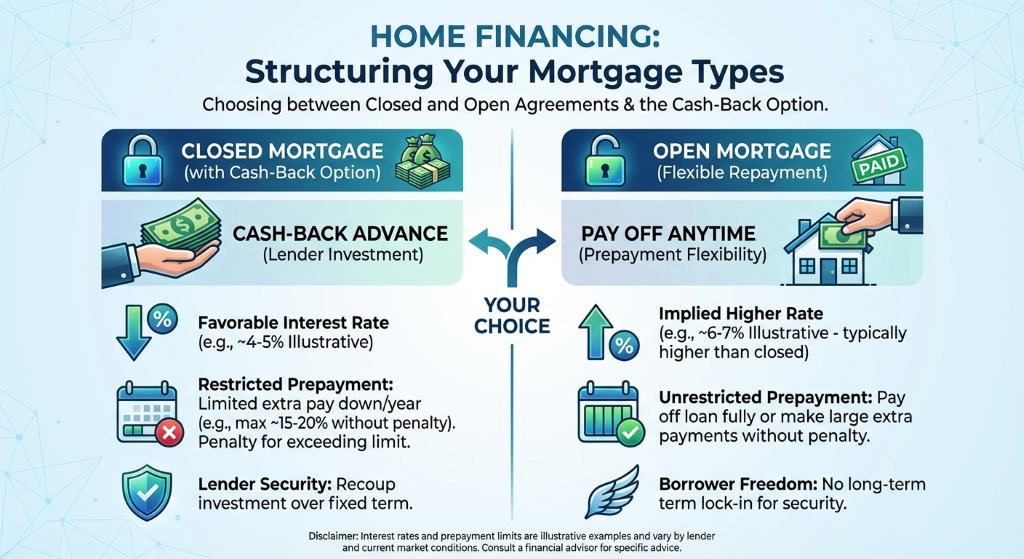

When structuring your home financing, you will need to choose between different mortgage types. A cash-back option is typically tied to a closed-mortgage. In a closed agreement, the interest rate is often more favorable, but you are restricted in how much extra you can pay down each year without incurring a penalty. Because the lender is advancing you cash up front, they need the security of a closed term to recoup their investment over time.

Conversely, an open-mortgage allows you to pay off your entire balance at any time without prepayment penalties. While open mortgages offer incredible flexibility, they rarely come with cash-back incentives and generally feature higher interest rates. For homeowners in Burlington, Oakville, and Hamilton, choosing the right path depends on your immediate cash needs versus your desire for payment flexibility.

Before signing any paperwork, it is vital to get a professional review. We are experts at providing second opinions on cash-back mortgages, ensuring you fully understand the clawback rules if you decide to break your mortgage early.

| Mortgage Feature | Cash-Back Mortgage | Closed-Mortgage | Open-Mortgage |

|---|---|---|---|

| Upfront Cash Provided | Yes (1% to 5% of loan) | No | No |

| Prepayment Flexibility | Low (Penalties apply) | Low to Moderate | High (No penalties) |

| Interest Rates | Slightly Higher Premium | Lower Standard Rates | Higher Standard Rates |

| Best For | Buyers needing upfront capital | Buyers seeking lowest rates | Buyers expecting a windfall |

Expert Advice for Burlington Homebuyers

Navigating the cash back mortgage Canada options can feel overwhelming, but you do not have to do it alone. As a dedicated Principal Broker serving Burlington, ON, and surrounding areas, Jason Woods is committed to finding the perfect financing solution for your unique needs. Whether you are a first-time homebuyer needing extra cash for closing costs or an existing homeowner looking into mortgage refinancing, expert guidance is just a phone call away.

It is important to note that if you break a cash-back mortgage early, lenders will often require you to repay a prorated portion of the cash you received. This is why having a professional broker review your contract is so important. We pride ourselves on being experts at providing second opinions on cash-back mortgages. We will carefully analyze your current offer, compare it with alternatives from over 40 lenders, and ensure you are making a sound financial decision.

Q1: What is a cash-back mortgage?

A cash-back mortgage, also known as a cashback mortgage, is a home loan that provides the borrower with a lump sum of cash at closing, typically ranging from one to five percent of the total mortgage amount.

Q2: Can I get a cash-back mortgage with an open-mortgage?

Generally, cash-back incentives are offered on a closed-mortgage. Lenders require the security of a closed term to ensure they recover the cost of the upfront cash advance over the life of the term.

Q3: What happens if I break my cash-back mortgage early?

If you refinance or pay off your loan before the term ends, you will typically face standard prepayment penalties plus a prorated clawback of the cash you received upfront. We highly recommend letting us provide a second opinion to explain these terms clearly.

Q4: How can I use the funds from a cashback mortgage?

The funds are entirely yours to use as you see fit. Common uses include paying for land transfer taxes, legal fees, moving expenses, purchasing new furniture, or consolidating high-interest debt.

Q5: Are cash back mortgages available in Burlington, ON?

Yes, they are widely available in Burlington and across the cash back mortgage Canada market. Jason Woods and TLC Mortgage Group can help you secure the best rates and terms from over 40 different lenders.

Ready to get the mortgage you deserve?

Contact Jason Woods, your Burlington Mortgage Broker, today for a free consultation or a second opinion on your mortgage offer.

Call 289-925-9599 Email Jason Woods