Mortgage Blog

Your Guide to Private Mortgages in Burlington and Across Canada

April 28, 2026 | Posted by: Matt Shepherd

Understanding Private Lenders and Equity Private Loans

When traditional banks say no, a private mortgage Canada residents can rely on might be the perfect solution. Private mortgages, also known as private lenders or equity private loans, offer alternative financing options for homeowners and buyers who need immediate flexibility. As a dedicated mortgage broker based in Burlington, ON, Jason Woods specializes in comprehensive coverage of non-bank mortgages and investor-funded private loans.

These alternative lending solutions are ideal for individuals looking for a bad credit mortgage or those who are self-employed and cannot provide traditional income verification. Similar to a hard money loan USA investors use, Canadian private mortgages focus heavily on the equity of the property rather than just the borrower's credit score.

- Fast Approvals: Private lenders often process applications much faster than major banks.

- Flexible Criteria: Approval is primarily based on property value and available equity.

- Short-Term Solutions: Perfect for bridge financing, home renovations, or debt consolidation.

Why Choose Investor-Funded Private Loans?

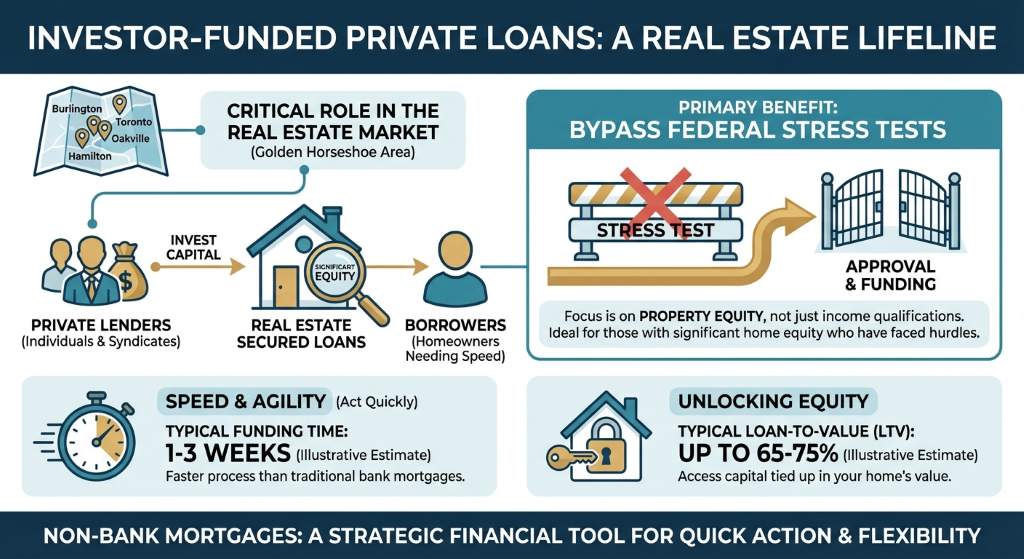

Investor-funded private loans serve a critical role in the real estate market. Whether you are in Burlington, Hamilton, Oakville, or Toronto, these non-bank mortgages provide a lifeline when you need to act quickly. Private lenders are typically individuals or syndicates looking to invest their capital into real estate secured loans.

One of the main benefits of an equity private loan is the ability to bypass strict federal stress tests. If you have significant equity in your home but have faced financial hiccups, a private mortgage can help you consolidate high-interest debt or finance an urgent property need. We are experts at providing second opinions on private mortgages. If you have received a quote from another lender, let Jason Woods review it to ensure you are securing the best possible terms.

| Feature | Traditional Bank Mortgage | Private Mortgage (Equity Loan) |

|---|---|---|

| Approval Time | 14 to 30 days | 3 to 7 days |

| Credit Score Requirement | Strict (Typically 680 and above) | Flexible (Focuses on Property Equity) |

| Income Verification | Extensive documentation required | Alternative or minimal verification |

| Typical Loan Term | 3 to 5 years | 1 to 2 years |

| Primary Approval Metric | Debt Service Ratios (GDS/TDS) | Loan-to-Value (LTV) Ratio |

Expert Second Opinions on Non-Bank Mortgages

Securing a private mortgage is a significant financial decision. Because private lenders operate differently than major financial institutions, the fees, interest rates, and terms can vary wildly. That is exactly why we are experts at providing second opinions on private mortgages. We review the fine print, assess the lender fees, and ensure your exit strategy aligns with your long-term financial goals.

As a licensed professional with TLC Mortgage Group (Lic. 12988), Jason Woods is committed to transparency and compliance in every transaction. Whether you need help with mortgage refinancing or are exploring investor-funded private loans for an investment property, you deserve unbiased, expert advice. Serving Burlington and surrounding areas, our goal is to build you a better mortgage strategy.

Q1: What is a private mortgage in Canada?

A private mortgage in Canada is a short-term, typically interest-only loan provided by an individual investor or a syndicate rather than a traditional bank. These loans focus primarily on the equity in your property instead of your credit history.

Q2: How do equity private loans differ from standard bank mortgages?

Equity private loans have more flexible qualification criteria, faster approval times, and rely on the property's overall value (Loan-to-Value ratio). Traditional bank mortgages require strict income verification and high credit scores.

Q3: Can I get a private mortgage with bad credit?

Yes, private lenders are often willing to provide a bad credit mortgage if you have sufficient equity in your home. They look at the big picture rather than just a three-digit credit score.

Q4: Why should I get a second opinion on a private mortgage offer?

Private mortgage terms, interest rates, and fees can vary significantly from one lender to another. An expert second opinion ensures you understand the costs, the renewal terms, and the exit strategy, potentially saving you thousands of dollars.

Q5: Are investor-funded private loans safe?

Yes, when facilitated by a licensed mortgage broker like Jason Woods, investor-funded private loans are secure and legally binding agreements. Working with a professional ensures all compliance and regulatory standards are met.

Contact Jason Woods for a Free Private Mortgage Consultation