Mortgage Blog

Your Guide to a Home Equity Loan and Second Mortgage in Burlington

April 28, 2026 | Posted by: Matt Shepherd

Understanding the Basics of a Second Mortgage in Canada

If you are a homeowner in Burlington, ON, looking to unlock the value of your property, a Home Equity Loan, also known as a Second Mortgage, might be the perfect financial solution. A second mortgage allows you to borrow against the equity you have built up in your home without touching your primary mortgage. This is an excellent tool for debt consolidation, home renovations, or major life expenses.

When exploring a second mortgage in Canada, it is crucial to understand your options. Whether you are in Burlington, Hamilton, or Oakville, we are experts at providing second opinions on home equity loans and second mortgages to ensure you get the best terms possible.

- Use your home equity to secure lower interest rates compared to high-interest credit cards.

- Maintain your current first mortgage rate without paying breaking penalties.

- Access funds quickly for immediate financial needs.

Depending on your financial goals, you might also want to explore a home equity line of credit (HELOC) or a private mortgage as alternative solutions.

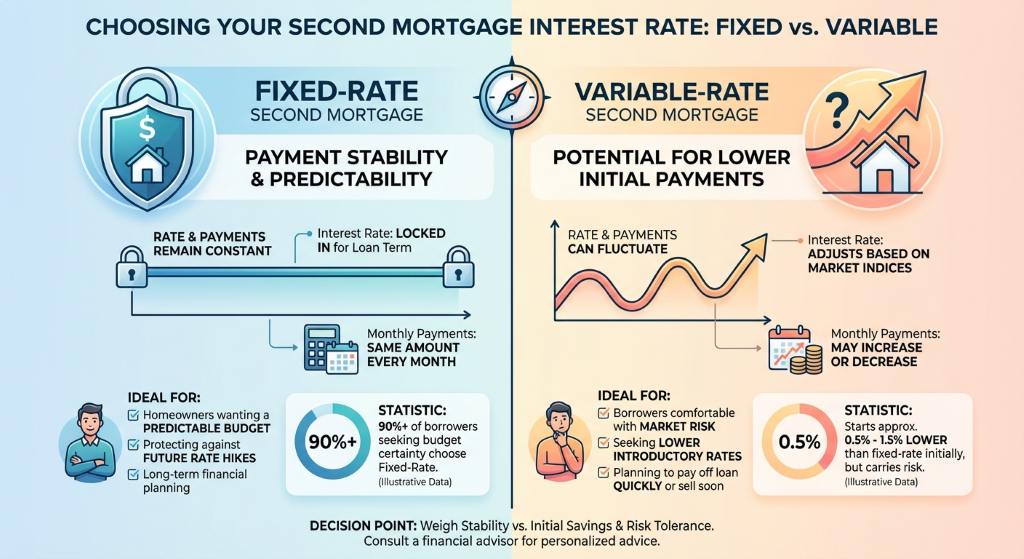

Fixed-Rate Second vs. Variable-Rate Second Mortgage

Choosing the right type of interest rate is a critical step when securing a second mortgage. Borrowers generally have two primary choices: a fixed-rate second mortgage and a variable-rate second mortgage.

A fixed-rate second mortgage provides payment stability. Your interest rate and monthly payments remain the same throughout the term of the loan. This option is ideal for homeowners who prefer a predictable budget and want to protect themselves against potential interest rate hikes.

Conversely, a variable-rate second mortgage fluctuates with the prime lending rate. While the initial rate is often lower than a fixed-rate option, your payments or the amount going toward the principal can change. This choice suits borrowers who can handle slight payment variations and want to take advantage of potentially lower rates in a stable or declining market.

| Feature | Fixed-Rate Second Mortgage | Variable-Rate Second Mortgage |

|---|---|---|

| Interest Rate | Locked in for the full term | Fluctuates with the prime lending rate |

| Payment Stability | Highly predictable monthly payments | Payments or principal amount can change |

| Risk Level | Lower risk against market changes | Moderate risk depending on economy |

| Best Suited For | Budget-conscious homeowners | Homeowners expecting rates to drop |

Why Choose Jason Woods for Your Burlington Second Mortgage Needs?

As a licensed Principal Broker (Lic. 12988) based at 1100 Burloak Dr in Burlington, ON, Jason Woods is dedicated to helping you navigate the complexities of home equity loans. We know that mortgages have changed, and getting the mortgage you deserve requires expert guidance.

We are experts at providing second opinions on home equity loans and second mortgages. If you have been quoted a rate from another lender, let us review it. With access to over 40 lenders, we can often find a more suitable product that aligns with your specific financial situation.

Our services extend proudly to Burlington, Hamilton, Oakville, and Toronto. From debt consolidation to funding property investments, leveraging your home equity has never been more secure and straightforward.

Q1: What is a second mortgage in Canada?

A second mortgage is an additional loan taken out on a property that already has a primary mortgage. It is secured against the equity you have built in your home.

Q2: What is the difference between a home equity loan and a HELOC?

A home equity loan provides a lump sum of money with a fixed repayment schedule. A home equity line of credit (HELOC) acts like a revolving credit line that you can borrow from and repay as needed.

Q3: Can I get a second mortgage with a bad credit score?

Yes, it is possible. Because the loan is secured by your property equity, private lenders are often more flexible with credit requirements compared to traditional banks.

Q4: How do I decide between a fixed-rate and a variable-rate second mortgage?

Your decision should be based on your risk tolerance and budget flexibility. A fixed-rate offers predictable payments, while a variable-rate can save you money if interest rates decrease.

Q5: Why should I get a second opinion on my home equity loan?

Getting a second opinion ensures you are not locked into unfavorable terms. As local Burlington mortgage experts, we review your current offers to see if we can secure a better rate or more flexible conditions for you.

Contact Jason Woods at 289-925-9599 for Your Free Second Opinion Today