Mortgage Blog

Your Complete Guide to Condo Financing and Strata Mortgages in Burlington

April 21, 2026 | Posted by: Matt Shepherd

Navigating a Condo Mortgage in Canada

Securing a condo mortgage in Canada involves a unique set of steps compared to buying a detached home. Whether you are looking at a sleek new build in downtown Burlington, ON, or a cozy unit in a well-established neighbourhood, understanding the ins and outs of condo financing (often referred to as strata financing) is critical to your success.

At Jason Woods Mortgages, we specialize in helping buyers navigate these waters. From understanding condo fees to securing the best rates, we are here to guide you. If you already have an offer from a lender, we are experts at providing second opinions on condo financing to ensure you get the most competitive deal available. Depending on your down payment, you might be considering a conventional fixed rate mortgage or you may need a high ratio insured mortgage (CMHC/Genworth). We will help you weigh the pros and cons of each option.

Warrantable Strata and Pre-Sale Condo Financing Explained

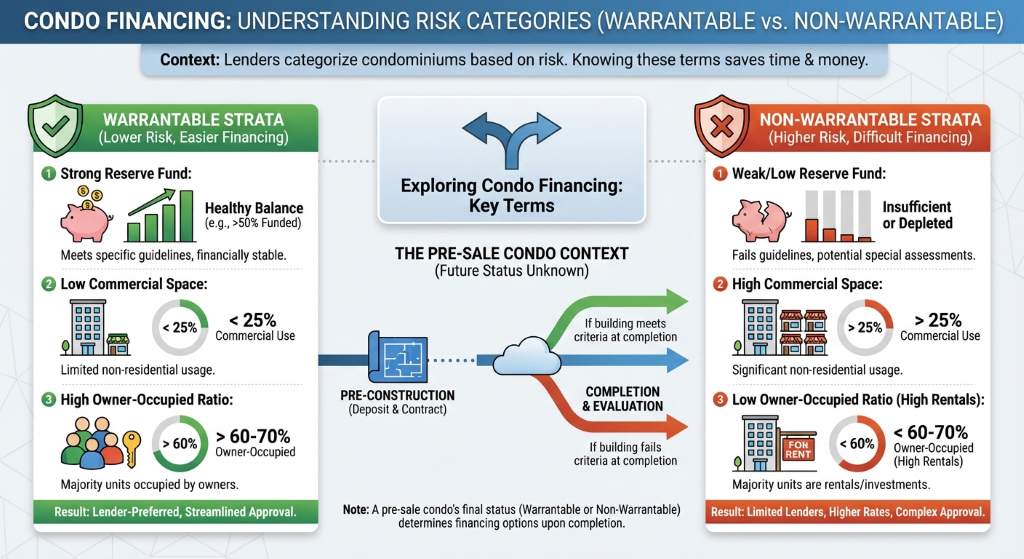

When exploring condo financing, two critical terms you will encounter are warrantable strata and pre-sale condos. Lenders categorize condominiums based on risk, and understanding these categories can save you time and money.

- Warrantable Strata: A warrantable condo meets specific lender guidelines, making it much easier to finance. These buildings typically have a strong reserve fund, a low percentage of commercial space, and a high ratio of owner-occupied units.

- Non-Warrantable Strata: If a building is under construction, operates as a condotel, or has ongoing litigation, lenders consider it non-warrantable. Financing these units requires specialized mortgage products.

- Pre-Sale Condos: Buying a condo before it is built is an excellent investment strategy in Burlington. However, pre-sale condo financing requires a firm mortgage approval that holds your rate until the building is registered.

Working with a knowledgeable Burlington mortgage broker ensures you secure the right financing for your specific property type.

| Property Type | Minimum Down Payment | CMHC Insurance Required? | Typical Rate Lock Period |

|---|---|---|---|

| Resale Condo (Under $500k) | 5% | Yes | 90 to 120 Days |

| Resale Condo ($500k to $999k) | 5% on first $500k, 10% on remainder | Yes | 90 to 120 Days |

| Pre-Sale Condo | Typically 15% to 20% (Deposit Structure) | Depends on final mortgage amount | Up to 36 Months (Builder Capped Rate) |

| Non-Warrantable Condo | 20% or more | No (Alternative Lending) | Varies by Lender |

Why Choose Jason Woods for Your Condo Mortgage Needs

As a Principal Broker with TLC Mortgage Group (Lic. 12988), Jason Woods is dedicated to providing tailored mortgage solutions for residents of Burlington and surrounding areas. We know that navigating a condo mortgage in Canada can feel overwhelming, especially with ever-changing strata rules and lender policies.

We pride ourselves on offering fast mortgage pre-approvals and access to over 40 lenders. Whether you are a first-time buyer or looking to invest in a pre-sale unit, we have the expertise to secure your financing. Remember, we are experts at providing second opinions on condo financing. Do not settle for the first rate you are offered; let us review your file and find you a better mortgage.

Q1: What is the minimum down payment for a condo mortgage in Canada?

For a condo priced under $500,000, the minimum down payment is 5%. For condos priced between $500,000 and $999,999, you need 5% on the first $500,000 and 10% on the remaining balance.

Q2: How do condo fees affect my mortgage approval?

Lenders factor in 50% of your monthly condo maintenance fees when calculating your debt service ratios. High condo fees can reduce the total mortgage amount you qualify for.

Q3: What makes a condo non-warrantable?

A condo may be deemed non-warrantable if it is a condotel, has a high percentage of commercial space, lacks a sufficient reserve fund, or is involved in active litigation.

Q4: Can I lock in a mortgage rate for a pre-sale condo?

Yes, many lenders offer long-term rate holds or builder capped rates for pre-sale condos, which can protect you from interest rate increases for up to 36 months while the building is constructed.

Q5: Why should I get a second opinion on my condo financing?

Different lenders have different rules regarding strata corporations and pre-sale appraisals. A second opinion ensures you are not overpaying on interest and that your financing structure aligns perfectly with your financial goals.

Contact Jason Woods at 289-925-9599 for Your Free Condo Mortgage Consultation Today