Mortgage Blog

Navigating the Non Resident Mortgage Canada Process: A Guide for Foreign Buyers

April 21, 2026 | Posted by: Matt Shepherd

Understanding Foreign-Buyer and Visa Holder Mortgages in Burlington

Securing a non resident mortgage canada can feel like a complex journey, especially with changing regulations and unique lending criteria. Whether you are living abroad and looking to invest in Canadian real estate, or you are currently working in the country and need comprehensive coverage of visa holder mortgages, getting the right advice is critical.

At Jason Woods Mortgages in Burlington, ON, we specialize in helping international clients and newcomers navigate the foreign-buyer mortgage landscape. We understand that standard lending guidelines do not always fit your unique situation. That is why we are experts at providing second opinions on foreign buyer and non-resident mortgages. If you have been turned down elsewhere or simply want to ensure you are getting the best terms, our team is here to help.

For those looking for stability, exploring a conventional fixed rate mortgage is often a great starting point. We guide visa holders and non-residents through the specific down payment requirements, tax implications, and documentation needed to make your Canadian homeownership dream a reality.

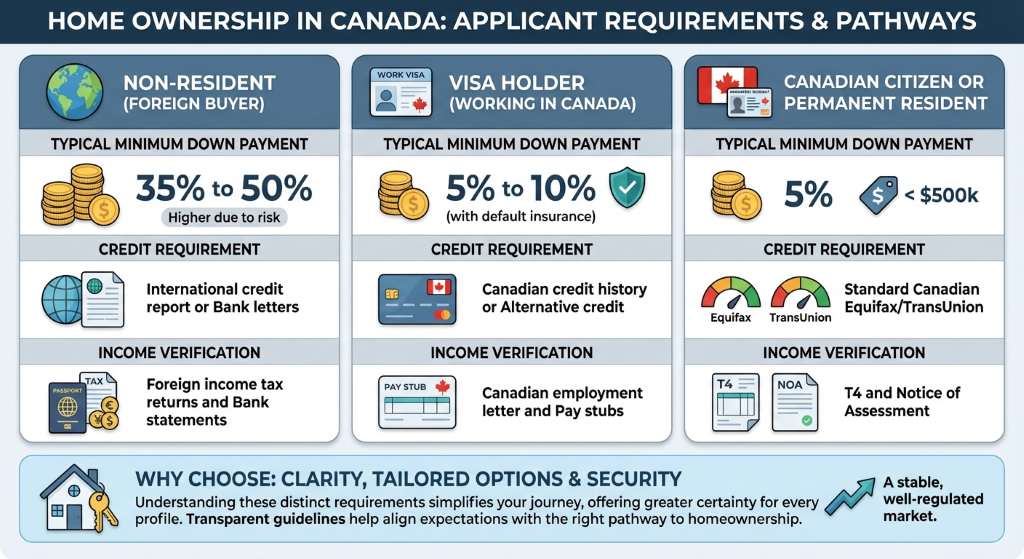

Key Requirements for a Non-Resident Mortgage in Canada

When applying for a non-resident mortgage, Canadian lenders look for specific criteria to mitigate their risk. Unlike local buyers, foreign investors and visa holders face distinct guidelines:

- Down Payment: Non-residents typically need a larger down payment, often ranging from 35% to 50% of the property purchase price. These funds must usually be traceable and sitting in a Canadian bank account for a specific period before closing.

- Credit Verification: Lenders will request an international credit report or alternative forms of credit history, such as letters of reference from your home bank.

- Income Proof: Comprehensive income verification is essential. For visa holder mortgages, lenders will look at your Canadian employment letter, work permit validity, and recent pay stubs.

Working with an experienced mortgage broker in Burlington ensures that you present a strong, organized application to the right lenders.

| Applicant Type | Typical Minimum Down Payment | Credit Requirement | Income Verification |

|---|---|---|---|

| Non-Resident (Foreign Buyer) | 35% to 50% | International credit report or Bank letters | Foreign income tax returns and Bank statements |

| Visa Holder (Working in Canada) | 5% to 10% (with default insurance) | Canadian credit history or Alternative credit | Canadian employment letter and Pay stubs |

| Canadian Citizen or Permanent Resident | 5% (up to $500k) | Standard Canadian Equifax/TransUnion | T4 and Notice of Assessment |

Why Choose Jason Woods for Your Foreign Buyer Mortgage?

Finding the right financing as a newcomer or overseas investor requires a broker who understands the nuances of the market. As a Principal Broker at TLC Mortgage Group (Lic. 12988), Jason Woods has built a reputation in Burlington and surrounding areas for delivering fast, simple, and secure financing solutions.

We pride ourselves on offering tailored advice. If you already have an offer from a bank, bring it to us. We are experts at providing second opinions on foreign buyer and non-resident mortgages, ensuring you are not leaving money on the table or accepting unfavorable terms. From navigating the Non-Resident Speculation Tax (NRST) in Ontario to finding lenders who welcome visa holder mortgages, we have access to over 40 lenders to secure the mortgage you deserve.

Q1: What is a non resident mortgage canada?

A non-resident mortgage is a home loan designed for individuals who do not live in Canada full-time or are not Canadian citizens or permanent residents, including foreign investors and temporary visa holders.

Q2: Can I get a mortgage in Canada on a work visa?

Yes, comprehensive coverage of visa holder mortgages is available. If you have a valid work permit and meet specific credit and income requirements, you can qualify for a mortgage, sometimes with a down payment as low as 5%.

Q3: How much down payment is required for a foreign buyer?

Typically, non-residents and foreign buyers are required to provide a down payment of 35% to 50% from their own resources, which must be verifiable in a Canadian bank account prior to closing.

Q4: Do you offer second opinions on non-resident mortgages?

Absolutely. We are experts at providing second opinions on foreign buyer and non-resident mortgages. We review your current pre-approval or denial to see if we can secure better rates or terms through our network of over 40 lenders.

Q5: Are there extra taxes for foreign buyers in Ontario?

Yes, foreign buyers purchasing property in regions like Burlington, ON, may be subject to the Non-Resident Speculation Tax (NRST). It is highly recommended to consult with a real estate lawyer to understand these specific tax implications.

Ready to secure your non-resident mortgage?

Contact Jason Woods today for expert advice and a free second opinion.

Email Jason Now Call 289-925-9599