Mortgage Blog

2026 Renewal Wave: Why 30% of Ontario Homeowners Could Save $300+/Month by Switching Early (And How to Time It)

March 17, 2026 | Posted by: Matt Shepherd

2026 Renewal Wave: Why 30% of Ontario Homeowners Could Save $300+/Month by Switching Early (And How to Time It)

The Looming 2026 Mortgage Cliff: What Burlington Homeowners Need to Know

If you secured a rock-bottom mortgage rate back in 2020 or 2021, you are part of a massive cohort approaching what financial experts call the 2026 mortgage renewal wave. Across Canada, billions of dollars in ultra-low fixed-rate mortgages are set to mature, and homeowners in Burlington, Oakville, and Hamilton are bracing for the payment shock.

However, the narrative that you simply have to accept a massive payment increase isn't entirely accurate. With the Bank of Canada making strategic shifts to its overnight lending rate, proactive homeowners are finding lucrative ways to soften the blow. By evaluating your mortgage renewal options ahead of time, data suggests that nearly 30% of Ontario homeowners could save upwards of $300 per month. The secret lies in understanding your mortgage penalty, tracking rate trends, and acting before your current term officially expires.

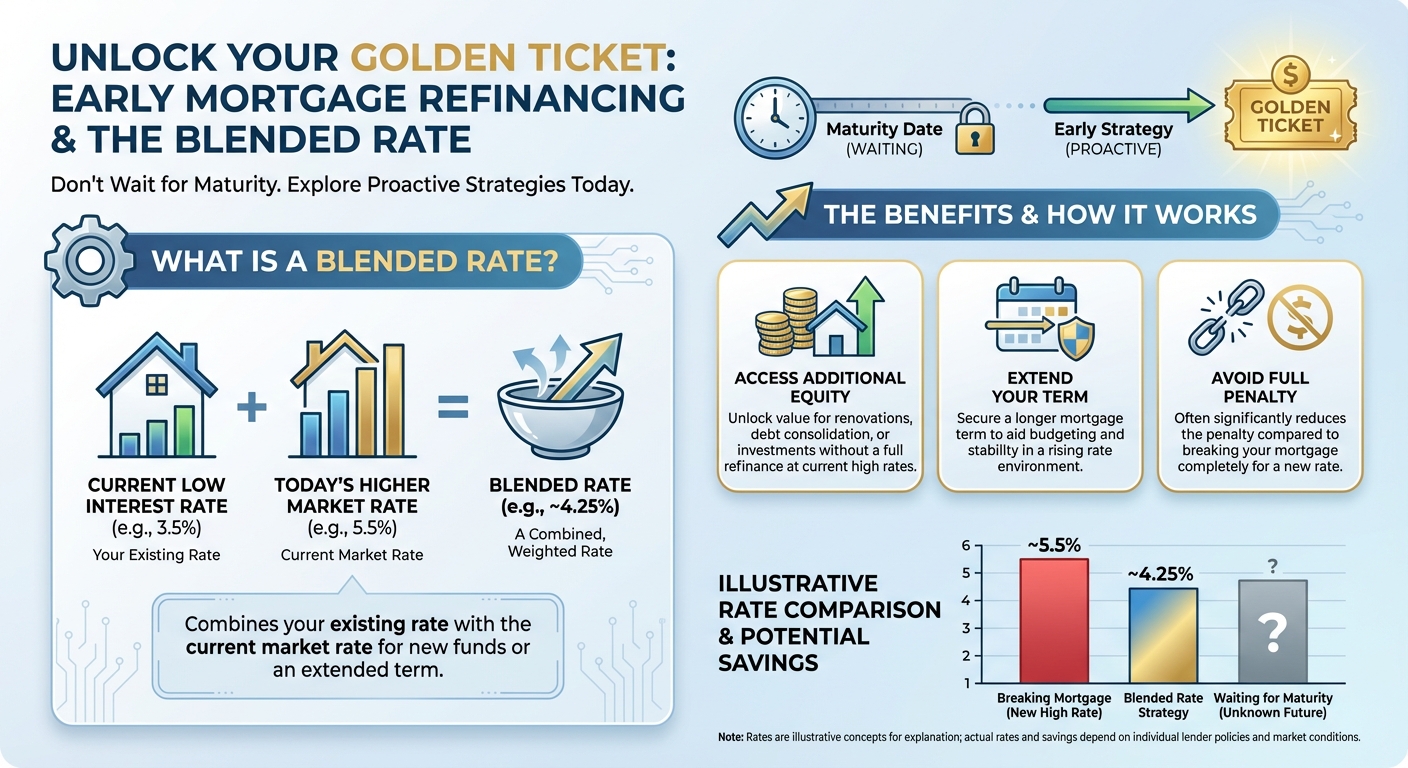

How Blended Rates and Early Renewals Can Save You Hundreds

Many homeowners assume they are stuck waiting until their maturity date, but exploring an early mortgage refinancing or renewal strategy could be your golden ticket. One of the most effective tools for navigating rising rates is the blended mortgage rate.

- What is a Blended Rate? A blended rate takes your current low interest rate and combines it with today's higher market rate. This allows you to access additional equity or extend your term without paying the full penalty of breaking your mortgage.

- The Early Switch Strategy: If market rates dip temporarily, breaking your mortgage early—even with a penalty—can sometimes save you thousands over the next five years compared to renewing at a potentially higher peak rate in 2026.

- Debt Consolidation: If you've accumulated high-interest consumer debt, rolling it into an early renewal can drastically reduce your overall monthly cash outflow.

As a dedicated Burlington mortgage broker, Jason Woods helps clients run the exact math to determine if the penalty of breaking early is outweighed by the long-term interest savings.

| Strategy | Current Rate (2021) | Projected 2026 Rate | Est. Monthly Payment ($500k Balance) | Potential Monthly Savings |

|---|---|---|---|---|

| Wait Until 2026 Maturity | 1.99% | 4.85% | $2,875 | $0 |

| Switch Early (Blended/Rate Drop Strategy) | 1.99% | 3.95% (Blended/Negotiated) | $2,550 | $325 |

Fixed vs. Variable: Timing the Bank of Canada Rate Shifts

With the Bank of Canada continuously adjusting rates to combat inflation, the age-old debate of fixed versus variable is more critical than ever. For those approaching the 2026 renewal wave, timing is everything.

If you opt to break early, choosing a variable rate might make sense if economists forecast further rate cuts leading into 2025 and 2026. Conversely, securing a shorter-term fixed rate (like a 3-year term) can provide stability now, allowing you to ride out the current economic volatility and renew again when rates have stabilized.

Working with an expert who has access to over 40 lenders ensures you aren't just taking the first renewal letter your current bank sends you. Remember, you can renegotiate everything pertaining to your mortgage. Don't waste time mortgage shopping alone when Jason Woods, Principal Broker, can verify your pre-approval quickly and secure the mortgage you deserve.

Q1: What is the 2026 mortgage renewal wave?

The 2026 mortgage renewal wave refers to the large number of Canadian homeowners who secured historically low 5-year fixed mortgage rates in 2020 and 2021. These terms will mature in 2025 and 2026, forcing borrowers to renew at today's higher interest rates.

Q2: Should I break my mortgage early before my 2026 renewal?

It depends on the math. If the Bank of Canada lowers rates temporarily, breaking your mortgage early to lock in a new rate could save you money over the long term, even after factoring in the prepayment penalty. A mortgage broker can run a cost-benefit analysis for your specific situation.

Q3: How does a blended mortgage rate work?

A blended rate combines your current low interest rate with the current market rate. This allows you to extend your mortgage term or access home equity without having to pay the full penalty associated with breaking your mortgage entirely.

Q4: Will my current bank offer me the best renewal rate?

Not usually. Banks often send renewal letters with posted rates that are higher than what you can get through a broker. Working with a Burlington mortgage broker like Jason Woods gives you access to over 40 lenders to ensure you get the most competitive rate.

Q5: How far in advance should I start planning for my mortgage renewal?

You should start reviewing your options at least 6 to 8 months before your maturity date. Some lenders allow you to lock in a new rate up to 120 days in advance, protecting you from potential rate hikes while you decide on your strategy.

Don't Wait for Your Bank's Renewal Letter

Discover how much you could save by restructuring your mortgage ahead of the 2026 wave. Let an expert do the shopping for you.

Get Your Free Mortgage Review TodayJason Woods, Principal Broker | TLC Mortgage Group | Lic. 12988

Call Now: 289-925-9599 | Serving Burlington & Surrounding Areas