Mortgage Blog

Beyond the Stress Test: The Hidden Affordability Math Ontario Buyers Miss in 2026

March 14, 2026 | Posted by: Matt Shepherd

Beyond the Stress Test: The Hidden Affordability Math Ontario Buyers Miss in 2026

Beyond the Stress Test: The Hidden Affordability Math Ontario Buyers Miss in 2026

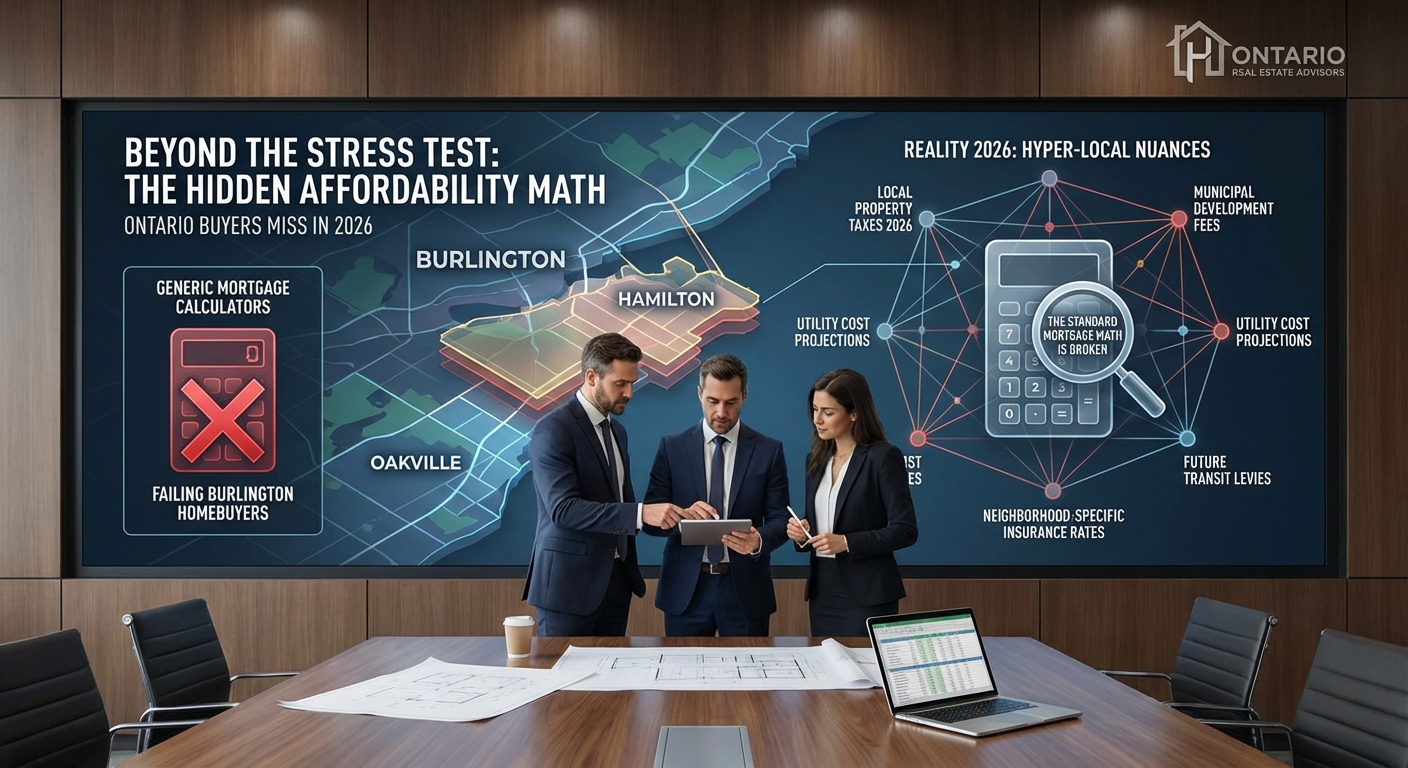

Why Generic Mortgage Calculators Are Failing Burlington Homebuyers

If you are planning to buy a home in Burlington, Hamilton, or Oakville in 2026, you've likely spent hours punching numbers into generic online calculators. But here is the reality: the standard mortgage math is broken.

While the federal stress test ensures you can handle interest rate fluctuations, it completely ignores the hyper-local nuances of the Ontario housing market. As a Burlington mortgage broker, I see firsthand how relying on basic formulas leaves buyers either dangerously stretched or needlessly restricted.

Generic calculators often miss the 'hidden affordability math' that lenders actually look at. This includes:

- Condo fees and their specific impact on your debt-service ratios.

- Accurate, localized property tax estimates for Burlington and surrounding areas.

- Heating costs and utility estimates based on property square footage.

- Future life-stage changes, like maternity leave or career transitions.

To truly maximize your buying power, you need advanced qualification modeling. That's where a professional mortgage pre-approval comes in.

Advanced Qualification Modeling: Unlocking Your True Buying Power

When lenders calculate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios, they aren't just looking at your principal and interest. They factor in the complete carrying cost of the property.

For example, if you are looking at first-time home buyer options in a Burlington condo, exactly 50% of your monthly condo fees are added to your debt load. A $600/month condo fee reduces your maximum mortgage amount significantly more than most buyers realize. Similarly, generic tools often use a blanket $100/month for heating costs, whereas lenders may use a different formula based on the property's size and age.

As your dedicated mortgage guide, I use advanced qualification modeling to build a comprehensive financial profile. By analyzing these hidden costs upfront, we can structure your application to position you favorably with over 40+ lenders. Sometimes, paying off a small $200/month car loan can increase your purchasing power by over $40,000. That is the kind of strategic, customized math that gets you into the home you deserve.

| Financial Variable | Generic Calculator Approach | Advanced Qualification Modeling |

|---|---|---|

| Condo Fees | Often ignored or underestimated | Exactly 50% factored into GDS/TDS ratios |

| Property Taxes | Uses provincial averages (inaccurate) | Uses precise Burlington/Hamilton municipal rates |

| Heating Costs | Flat $100/month estimate | Calculated based on property size/type |

| Consumer Debt | Subtracts debt 1:1 from income | Strategically consolidated to maximize buying power |

Navigate 2026 With Confidence: Partner With a Burlington Mortgage Expert

The Ontario real estate market in 2026 requires more than just a passing grade on the stress test; it requires a tailored financial strategy. Whether you are looking into mortgage refinancing to consolidate debt or buying your dream home, having an expert run the real numbers is crucial.

I proudly serve Burlington, Oakville, Hamilton, and Toronto, offering fast, simple, and secure financing solutions. Let's look beyond the stress test and uncover your true affordability.

Compliance Notice: Jason Woods is the Principal Broker at TLC Mortgage Group | Lic. 12988. Proudly serving Burlington and surrounding areas.

Q1: Why is the mortgage stress test not enough to determine my true affordability?

The stress test only ensures you can afford higher interest rates, but it ignores local property taxes, condo fees, and heating costs that directly impact your monthly budget and lender qualification limits.

Q2: How do condo fees affect my mortgage pre-approval in Ontario?

Lenders calculate exactly 50% of your monthly condo fees into your Gross Debt Service (GDS) ratio. High condo fees can drastically reduce the total mortgage amount you qualify for.

Q3: Should I pay off my car loan before applying for a mortgage?

Often, yes. Eliminating a monthly debt payment like a car loan can significantly lower your Total Debt Service (TDS) ratio, sometimes increasing your purchasing power by tens of thousands of dollars.

Q4: Can upcoming life-stage changes impact my mortgage qualification in 2026?

Absolutely. Upcoming changes such as maternity leave, career shifts, or retirement plans must be factored into advanced qualification modeling to ensure you aren't stretched too thin in the future.

Q5: Why should I use a mortgage broker instead of my bank?

As a licensed broker with TLC Mortgage Group, I have access to over 40 lenders. I use advanced modeling to find the best rates and terms customized to your exact financial situation, which a single bank cannot offer.

Get Your Advanced Pre-Approval Today