Mortgage Blog

Building Your Mortgage Like a Portfolio: Lessons From 10+ Years That Turn Debt Into Long-Term Wealth

March 25, 2026 | Posted by: Matt Shepherd

Shift Your Mindset: Why Your Mortgage is an Asset Management Tool

For most homeowners in Burlington, ON, a mortgage is often viewed simply as a necessary monthly expense—a massive debt to be paid off over 25 years. But after spending more than a decade helping clients navigate the real estate market, I have learned a critical secret: the wealthiest homeowners do not see their mortgage as a burden. Instead, they treat it like a dynamic financial portfolio.

When you start managing your mortgage with the same forward-thinking strategy you apply to your retirement savings, you can effectively turn your debt into long-term wealth. Whether you are looking at mortgage refinancing to unlock equity, or utilizing strategic prepayment privileges, your mortgage is one of the most powerful asset management tools at your disposal. As a dedicated mortgage broker serving Burlington, Hamilton, Oakville, and Toronto, my goal is to help you actively manage this asset.

Strategic Amortization and Prepayment Privileges

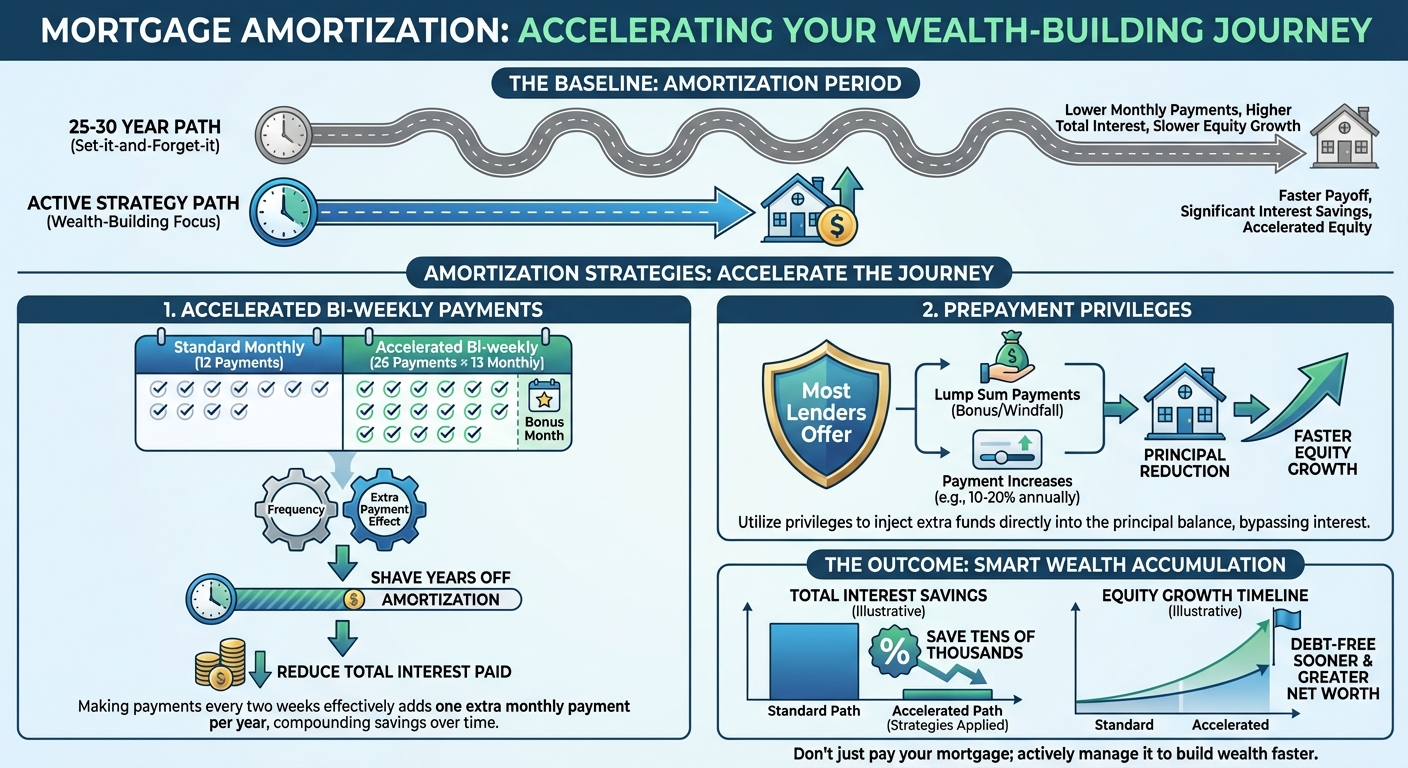

When you secure a mortgage, your amortization period sets the baseline for your wealth-building journey. While a 25-year or 30-year amortization offers lower monthly payments, it should never be a set-it-and-forget-it sentence.

- Amortization Strategies: By opting for an accelerated bi-weekly payment schedule, you effectively make one extra monthly payment per year. This simple shift can shave years off your total amortization and reduce the total interest paid.

- Prepayment Privileges: Most lenders allow you to prepay up to 15% or 20% of your original mortgage principal each year without penalty. Treat this like a guaranteed, tax-free return on investment. Every extra dollar you put toward your principal directly reduces the interest calculated on your next payment.

As an experienced Burlington mortgage broker, I always advise clients to review their prepayment options annually. Putting your year-end bonus or tax return toward your mortgage can drastically shift the math in your favor.

Payment Strategy Comparison| Payment Strategy | Payment Amount | Estimated Interest Saved | Time to Pay Off (from 25 Yrs) |

|---|---|---|---|

| Standard Monthly (Baseline) | $2,900 / month | $0 | 25 Years |

| Accelerated Bi-Weekly | $1,450 / every 2 weeks | $55,000+ | 21.5 Years |

| Accelerated + $5K Annual Prepayment | $1,450 / every 2 weeks + $5k/yr | $125,000+ | 17 Years |

Timing Your Refinance: Unlocking Equity for Growth

Another crucial element of building your mortgage like a portfolio is knowing when to restructure. Mortgage refinancing is not just for emergencies; it is a calculated move to optimize your financial standing and leverage your property's equity.

Here is how forward-thinking homeowners use refinancing to their advantage:

- Debt Consolidation: Rolling high-interest consumer debt (like credit cards or auto loans) into your lower-rate mortgage improves your monthly cash flow, allowing you to redirect those funds into wealth-building investments. Learn more about your debt consolidation options.

- Funding Investment Properties: As your Burlington property appreciates, you build equity. You can refinance to pull out this equity and use it as a down payment on an investment property, diversifying your assets and creating passive income streams.

- Home Renovations: Reinvesting in your primary residence through renovation financing can significantly increase its market value, yielding a high return when it comes time to sell or appraise.

Timing is everything. Keeping an eye on interest rate trends and your home's appraised value ensures you strike when the market is favorable. With access to over 40 lenders, I help my clients monitor these conditions to make the best financial moves.

Q1: What does it mean to treat a mortgage like a portfolio?

It means actively managing your mortgage through strategic prepayments, refinancing, and amortization adjustments to build equity and minimize interest, rather than just passively making monthly payments.

Q2: Are there penalties for paying off my mortgage faster?

Most lenders offer prepayment privileges allowing you to pay down 10% to 20% of the principal annually without penalty. Always check your specific mortgage contract or consult with your mortgage broker to understand your limits.

Q3: When is the best time to refinance my mortgage?

The ideal time to refinance is when interest rates drop significantly, when you have built substantial equity to invest elsewhere, or when you need to consolidate high-interest debt to improve your monthly cash flow.

Q4: How does an accelerated bi-weekly payment save me money?

By paying half your monthly payment every two weeks, you end up making 26 half-payments a year, which equates to 13 full months. This extra full payment goes directly to the principal, reducing the life of your mortgage and the total interest paid.

Q5: Can Jason Woods help me if I live outside of Burlington?

Yes! While I am based in Burlington, ON, I proudly serve clients across Hamilton, Oakville, Toronto, and the surrounding areas, providing expert mortgage advice tailored to your long-term financial goals.

Ready to turn your mortgage into a powerful wealth-building tool? Let an expert do the heavy lifting for you.

Contact Jason Woods Today at 289-925-9599