Mortgage Blog

New-to-Canada Mortgages in Ontario: Beyond the 35% Rule

March 24, 2026 | Posted by: Matt Shepherd

Strategies for Immigrants to Build Equity Faster in Burlington and Beyond

Welcome to Canada! If you've recently moved to Ontario and are looking to put down roots, buying a home is likely at the top of your list. For many newcomers, securing a mortgage can feel like navigating a maze, especially with the widely discussed 35% down payment rule. However, as a dedicated mortgage broker in Burlington, ON, I'm here to tell you that there are flexible, strategic alternatives available.

While the standard New-to-Canada mortgage programs often require a hefty 35% down payment if you lack a Canadian credit history, this isn't the only path to homeownership. By leveraging non-resident credit, gifted down payments, and the right lender flexibility, immigrants can build equity faster than they might think. Let's explore how you can bypass traditional barriers and secure the New To Canada mortgage you deserve.

Navigating Non-Resident Credit and Gifted Down Payments

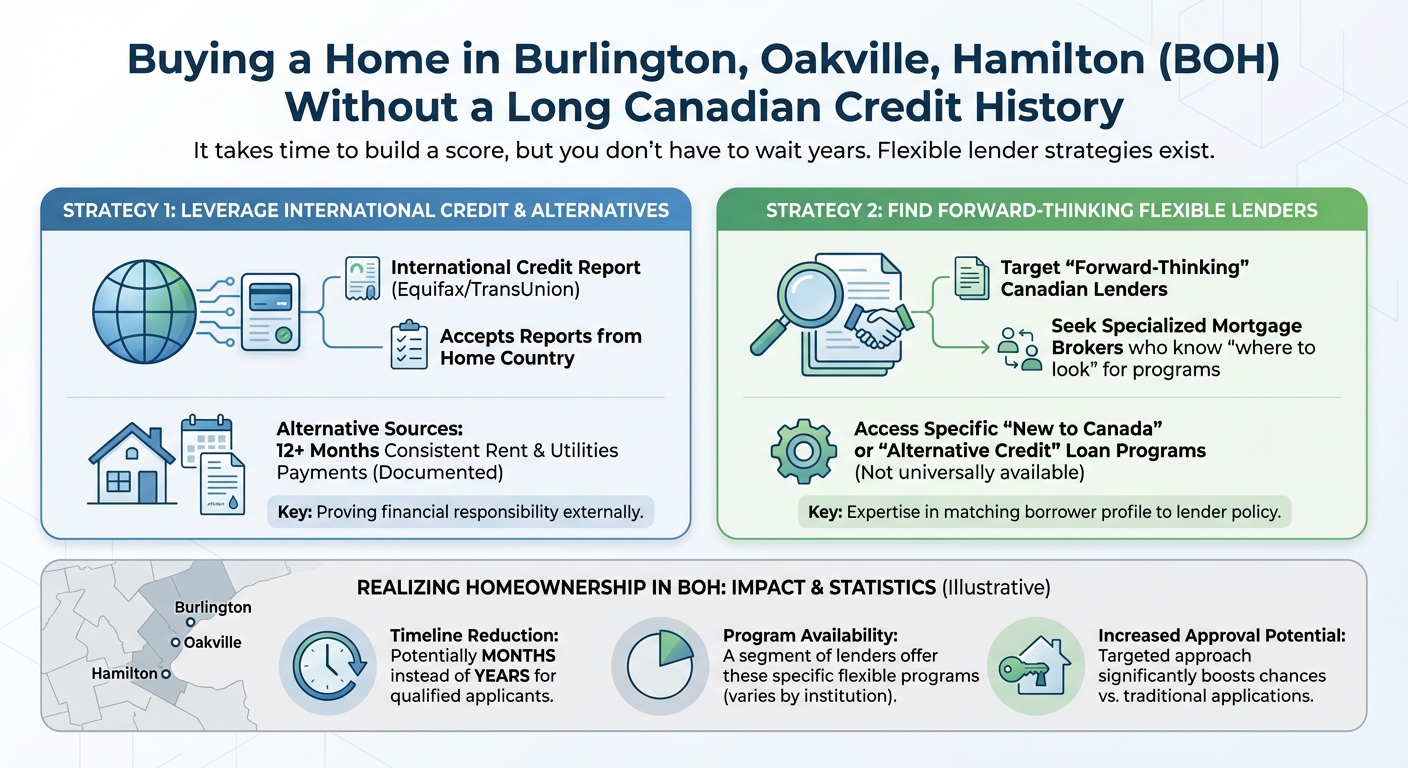

Building a Canadian credit score takes time, but you don't necessarily have to wait years to buy a home in Burlington, Oakville, or Hamilton. Many lenders offer incredible flexibility if you know where to look. Here are some of the most effective strategies:

- Leveraging International Credit: Some forward-thinking Canadian lenders will accept an international credit report (like Equifax or TransUnion from your home country) or alternative credit sources, such as 12 months of consistent rent and utility payments.

- Gifted Down Payments: If you don't have the full 35% saved up, many lenders allow a portion (or sometimes all) of your down payment to be gifted by an immediate family member. This is a powerful tool for first-time home buyers.

- Work Permits and Corporate Relocation: If you are in Ontario on a valid work permit or were relocated by your employer, you may qualify for a mortgage with as little as 5% down, provided you meet specific income and employment criteria.

Working with a broker who has access to over 40 lenders means we can match your unique financial profile with a lender who understands newcomer nuances. Getting a fast mortgage pre-approval is your first step to understanding exactly what you qualify for.

| Down Payment Amount | Credit History Requirement | Typical Source of Funds | Lender Flexibility |

|---|---|---|---|

| 5% - 19.99% | Strong Canadian or Alternative Credit (e.g., International report, 12-mo rent history) | Personal savings or gifted from immediate family | Requires default insurance (CMHC, Sagen, Canada Guaranty) |

| 20% - 34.99% | Moderate Canadian Credit or Alternative Credit | Personal savings or gifted funds | Uninsured options available; flexible income verification |

| 35% or more | No minimum Canadian credit history required | Personal savings (must be in Canada for 30-90 days) | Highly flexible; standard New-to-Canada program |

Why Work With a Specialized Burlington Mortgage Broker?

As an immigrant, your financial situation is unique. Walking into a big bank might result in a swift rejection simply because you don't fit into their rigid, automated algorithms. As a specialized mortgage broker serving Burlington, Hamilton, and Toronto, I partner with lenders who share my belief that applying for a mortgage should be fast, simple, and secure.

Why choose my services?

- Access to 40+ Lenders: I shop the market so you don't have to, ensuring you get the most competitive rates and terms.

- Tailored Strategies: Whether you need help with credit improvement or navigating a gifted down payment, I provide nuanced advice tailored to newcomers.

- Speed and Convenience: Speed matters when it comes to your next home. I help verify your pre-approval quickly so you can make an offer with confidence.

Jason Woods is a Principal Broker with TLC Mortgage Group (Lic. 12988), dedicated to helping you get the mortgage you deserve today.

Q1: Do I need a 35% down payment to buy a house as a newcomer to Canada?

Not necessarily. While the 35% rule is common for those with zero credit history, alternative credit sources, work permits, and gifted down payments can allow you to purchase with as little as 5% down.

Q2: Can I use my credit history from my home country to get a mortgage in Ontario?

Yes, some Canadian lenders and mortgage insurers will accept an international credit report (such as Equifax or TransUnion) or alternative credit references like 12 months of rent and utility receipts.

Q3: Are gifted down payments allowed for New-to-Canada mortgages?

Absolutely. Many lenders allow immediate family members to gift you the funds for a down payment, which is a great strategy to build equity faster.

Q4: How long do I need to be employed in Canada before applying for a mortgage?

Typically, lenders like to see 3 months of full-time employment to ensure you've passed your probationary period. However, exceptions exist for corporate relocations or highly specialized fields.

Q5: Why should a newcomer use a mortgage broker instead of a bank?

A mortgage broker like Jason Woods has access to over 40 lenders, including specialized institutions that offer flexible policies for newcomers. Banks only offer their own rigid products, which may not suit an immigrant's unique financial profile.

Contact Jason Woods Today to Start Your Home Journey