Mortgage Blog

Investment Property Mortgages in the 905: Structuring for Cash Flow & Tax Efficiency in 2026

March 24, 2026 | Posted by: Matt Shepherd

The 2026 Landscape for Real Estate Investors in Burlington & The 905

Investing in real estate across the 905 region—especially in Burlington, Hamilton, and Oakville—continues to be a powerful wealth-building strategy. As we look toward 2026, the market for multi-unit homes, long-term rentals, and side-hustle properties requires a strategic approach to financing. It is no longer just about securing a property; it is about structuring your investment property mortgage to maximize monthly cash flow and optimize tax efficiency.

Whether you are blending personal and investment financing or leveraging equity from your primary residence, working with an experienced principal mortgage broker is crucial. Proper structuring can mean the difference between a property that drains your resources and one that funds your retirement.

- Maximize Cash Flow: Secure rates, terms, and amortizations that keep your monthly obligations low and your net rental income high.

- Tax Efficiency: Structure your debt properly so that interest payments become valuable tax-deductible expenses.

- Portfolio Growth: Strategically use equity from existing properties through mortgage refinancing to fund future acquisitions.

Let's explore how to position your real estate portfolio for lasting success in 2026.

Strategies for Multi-Unit Properties and Blended Financing

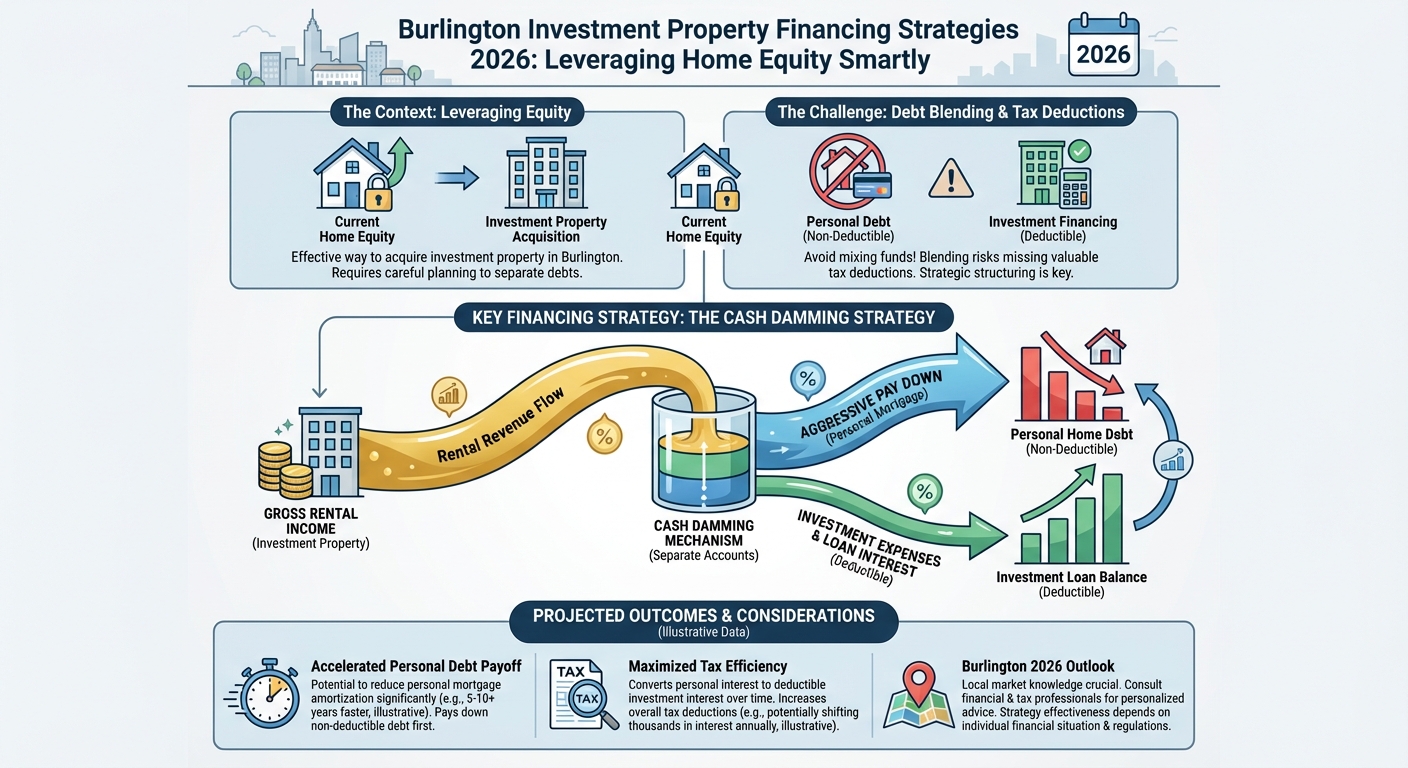

One of the most effective ways to acquire an investment property in the Burlington area is by leveraging the equity in your current home. However, blending personal debt with investment financing requires careful planning to ensure you do not miss out on valuable tax deductions.

Here are the key financing strategies to consider for 2026:

- The Cash Damming Strategy: This involves using the gross rental income from your investment property to aggressively pay down your non-deductible personal mortgage, while using a readvanceable line of credit to pay for the rental's operating expenses. Over time, this converts your 'bad debt' into tax-deductible 'good debt.'

- Using a HELOC for Down Payments: By separating your borrowed investment funds from your personal funds, the interest on the borrowed down payment remains tax-deductible. Always keep a clear paper trail to satisfy the CRA!

- Corporate vs. Personal Ownership: Depending on your income bracket, holding a multi-unit rental in a corporation might offer tax deferral benefits. It is essential to consult with both your mortgage broker and a tax professional to align your mortgage structure with your corporate setup.

When dealing with multi-unit properties, lenders will often use a portion of the projected rental income to help you qualify for the mortgage. Knowing exactly how different lenders calculate this 'rental offset' is where having access to over 40 lenders truly pays off.

Mortgage Comparison| Feature | Primary Residence Mortgage | Investment Property Mortgage |

|---|---|---|

| Minimum Down Payment | 5% (up to $500k), then 10% | 20% (Standard for non-owner occupied) |

| Interest Tax Deductibility | No (Under standard Canadian tax law) | Yes (Deductible against rental income) |

| Interest Rates | Standard Market Rates | Typically 0.10% - 0.25% higher |

| Income Qualification | Personal Income Only | Personal Income + % of Rental Income |

Why Work with a Local Burlington Mortgage Broker for Your Investments?

Navigating the complexities of investment property mortgages requires more than just a quick online search. It requires a deep understanding of the local market dynamics in Burlington, Hamilton, and Oakville. As the Principal Broker at TLC Mortgage Group (Lic. 12988), I, Jason Woods, specialize in helping investors structure their financing to align with their long-term wealth goals.

Why rely on a local expert?

- Access to 40+ Lenders: Not all banks treat rental income the same. I find the lenders whose underwriting policies work in your favor, maximizing your borrowing power.

- Fast Pre-Approvals: Speed matters in real estate. I ensure your mortgage pre-approval is solid so you can bid on that lucrative duplex with confidence.

- Holistic Financial Planning: From debt consolidation to optimizing cash flow across multiple properties, I look at your entire financial picture.

Whether you are buying your first side-hustle rental or adding a fifth multi-unit property to your portfolio, getting the structure right today will dictate your cash flow and tax efficiency in 2026 and beyond.

Q1: What is the minimum down payment for an investment property in Ontario?

For a non-owner-occupied investment property, the minimum down payment is strictly 20%. However, if you plan to live in one unit of a multi-unit property (up to 4 units) and rent out the others, you may qualify for a lower down payment as an owner-occupier.

Q2: Can I use projected rental income to qualify for my mortgage?

Yes, most lenders allow you to use a portion of the projected or actual rental income (typically 50% to 100%, depending on the specific lender's policies and the property type) to help you qualify for the investment property mortgage.

Q3: Is mortgage interest on a rental property tax-deductible in Canada?

Yes, the interest paid on a mortgage for an investment property is generally tax-deductible against the rental income generated by that property, which is a key strategy for improving your overall tax efficiency.

Q4: Should I buy my investment property under my personal name or a corporation?

This depends heavily on your personal income tax bracket, liability concerns, and long-term investment goals. While corporate ownership can offer tax deferral benefits, it often comes with slightly higher commercial mortgage rates and stricter qualification rules. Always consult a tax professional alongside your mortgage broker.

Q5: How can a HELOC help me buy an investment property?

A Home Equity Line of Credit (HELOC) allows you to borrow against the existing equity in your primary residence to fund the 20% down payment for an investment property. The interest on the borrowed funds used specifically for investing is typically tax-deductible.

Ready to Optimize Your Real Estate Portfolio?

Stop wasting time mortgage shopping and let an expert structure your financing for maximum cash flow.

Schedule Your Free Investment Strategy SessionOr call Jason Woods directly at 289-925-9599