Mortgage Blog

Cash-Out Refinancing in 2026: Unlocking Home Equity for Renovations, Investments, or Debt Consolidation

March 7, 2026 | Posted by: Matt Shepherd

Is Your Home Equity Working for You?

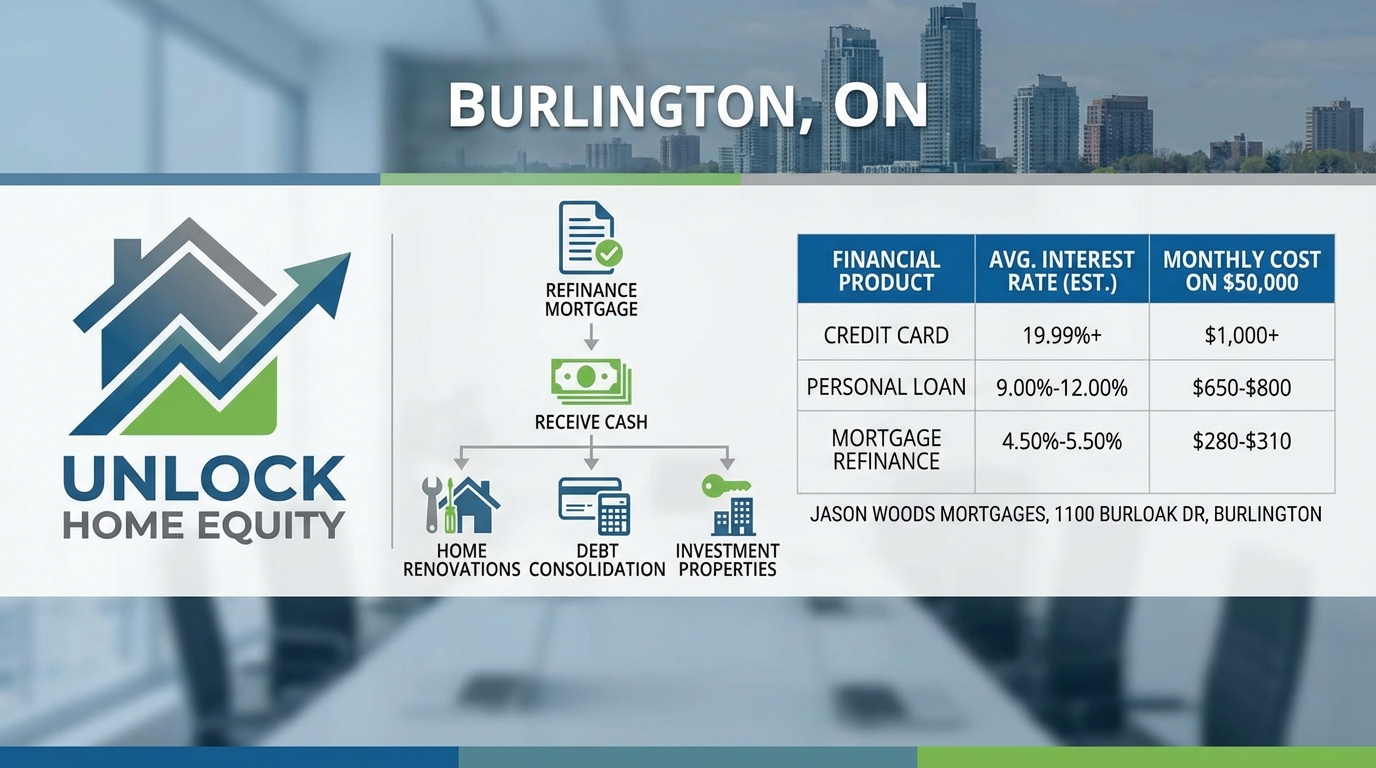

As we move through 2026, many homeowners in Burlington, ON, and the surrounding areas find themselves in a unique position. Property values have remained resilient, meaning you likely have significant equity built up in your home. Instead of letting that value sit idle, cash-out refinancing allows you to access up to 80% of your home's appraised value to fund major life goals.

Whether you are looking to update your property, pay off high-interest debt, or expand your real estate portfolio, refinancing can be a powerful financial tool. As a local Burlington Mortgage Broker, I help homeowners navigate these options to ensure they secure the best rates and terms available.

Strategic Ways to Use Your Equity

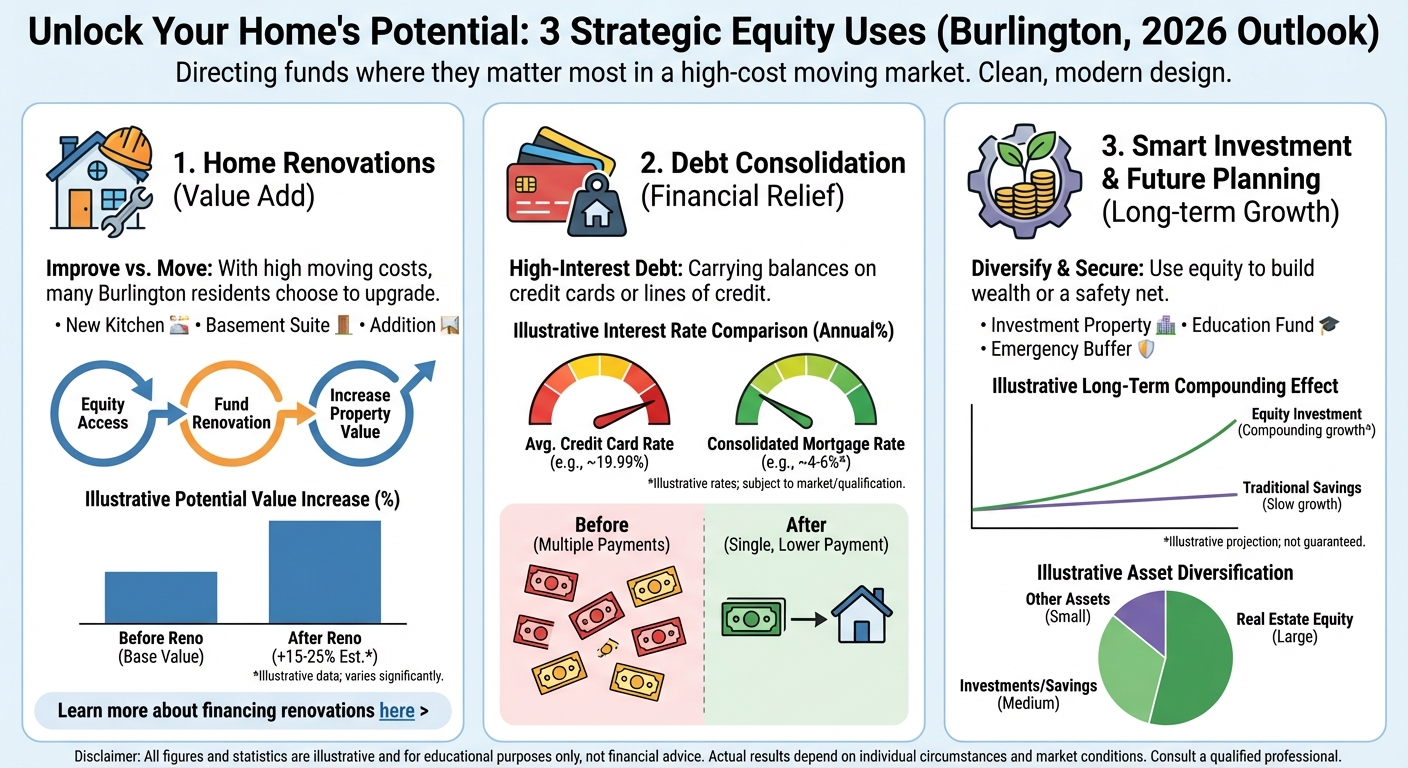

Unlock the potential of your home by directing funds where they matter most. Here are the three most common strategies for 2026:

- Home Renovations: With the cost of moving remaining high, many Burlington residents are choosing to improve rather than move. Accessing equity can fund a new kitchen, a basement suite, or an addition, which in turn increases your property value. Learn more about financing renovations here.

- Debt Consolidation: If you are carrying high-interest credit card debt or lines of credit, rolling them into a lower-interest mortgage payment can save you hundreds of dollars monthly. Visit our debt consolidation page to see how this works.

- Investment Properties: 2026 presents new opportunities in the real estate market. Using existing equity as a down payment for an investment property is a classic wealth-building strategy.

| Financial Product | Average Interest Rate (Est.) | Monthly Cost on $50,000 |

|---|---|---|

| Credit Card | 19.99% + | $1,000+ (Interest heavy) |

| Personal Loan | 9.00% - 12.00% | $650 - $800 |

| Mortgage Refinance | 4.50% - 5.50% | $280 - $310 |

The Refinancing Process with a Local Expert

Refinancing is more than just a transaction; it is a restructuring of your financial future. The process typically involves a new appraisal of your home to establish its current market value. In Canada, you can generally refinance up to 80% of this value, minus your remaining mortgage balance.

At Jason Woods Mortgages, located at 1100 Burloak Dr, Burlington, we streamline this process. We compare rates from over 40 lenders to ensure you aren't just getting cash out, but also securing a mortgage product that fits your long-term goals. Before you start, you can use our mortgage calculators to estimate your payments.

Q1: What is the maximum amount I can withdraw through cash-out refinancing?

In Canada, you can typically refinance up to 80% of your home's appraised value. The cash-out amount is the difference between that 80% limit and your current mortgage balance.

Q2: Are there penalties for breaking my current mortgage to refinance?

Yes, if you refinance before your term is up, you may face a prepayment penalty. However, the long-term savings from debt consolidation often outweigh this cost. We can calculate this for you.

Q3: How long does the refinancing process take in Burlington?

Generally, the process takes between 2 to 4 weeks, depending on how quickly an appraisal can be scheduled and documents are provided.

Q4: Can I use cash-out refinancing for a vacation home?

Absolutely. Many clients use the equity from their primary residence in Burlington to fund the down payment on a vacation home or cottage.

Q5: Does refinancing hurt my credit score?

There is a temporary dip due to the hard credit inquiry, but paying off high-interest credit card debt with the proceeds usually improves your score significantly in the long run.

Contact Jason Woods Today to Discuss Your Refinancing Options