Mortgage Blog

The Ultimate Guide to Refinancing Your Mortgage in 2026: Timing, Benefits, and Strategies Amid Stabilizing Rates

March 7, 2026 | Posted by: Matt Shepherd

Is 2026 the Right Time to Refinance Your Burlington Home?

As we navigate the financial landscape of 2026, homeowners in Burlington and across Ontario are witnessing a shift in the lending environment. With interest rates stabilizing after years of volatility, many property owners are asking: Is now the time to restructure my mortgage? Mortgage refinancing is more than just securing a lower rate; it is a strategic financial move that can unlock equity, lower monthly payments, and provide stability for the future.

Refinancing involves breaking your current mortgage agreement to start a new one, ideally with better terms. Whether you are looking to access cash for home renovations to increase your property value in the competitive Burlington market, or you want to consolidate high-interest debt, understanding the timing is crucial. As a Principal Broker serving Burlington and surrounding areas, I help clients analyze the cost-benefit ratio of breaking a term versus the long-term savings of a new rate environment.

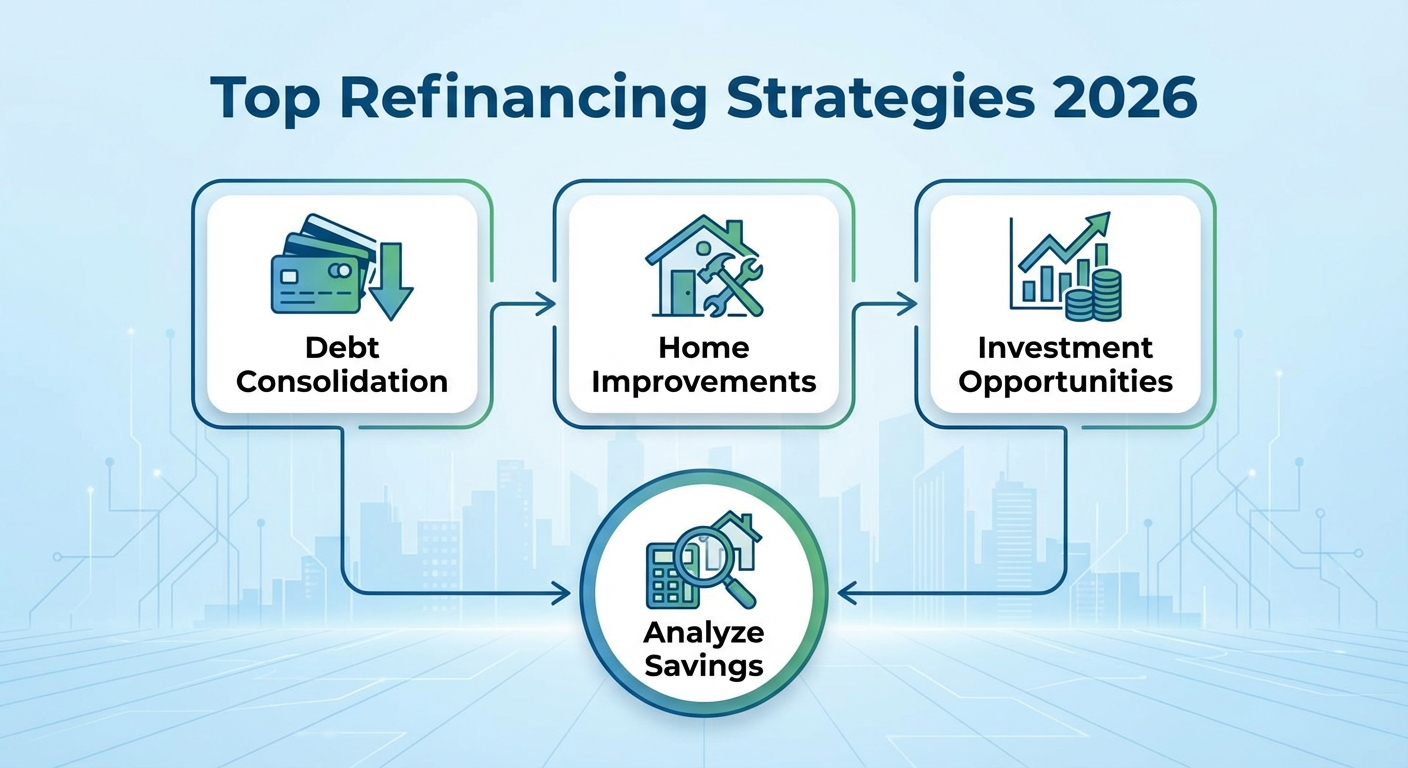

Top Strategies for Mortgage Refinancing in Ontario

When considering refinancing, it is essential to have a clear goal. In 2026, the most effective strategies often revolve around leveraging your home's equity to improve your overall financial health. Here are the primary reasons Burlington homeowners are choosing to refinance this year:

- Debt Consolidation: High-interest credit cards and lines of credit can be crippling. By rolling these debts into your mortgage at a significantly lower rate, you can reduce your total monthly outgoing cash flow. Learn more about debt consolidation options.

- Home Improvements: With housing inventory tight, many are choosing to improve rather than move. Accessing equity can fund major renovations that boost resale value.

- Investment Opportunities: Savvy homeowners are using equity to fund down payments for investment properties.

Before proceeding, it is vital to use mortgage calculators to estimate your potential savings and ensure the move aligns with your long-term goals.

| Financial Obligation | Interest Rate (Avg) | Monthly Payment | After Refinancing (Est.) |

|---|---|---|---|

| Credit Cards ($20k balance) | 19.99% | $600+ (Min + Interest) | Included in Mortgage |

| Car Loan ($30k balance) | 8.50% | $550 | Included in Mortgage |

| Current Mortgage | 5.25% | $2,400 | -- |

| New Refinanced Mortgage | 4.50% (Blended) | -- | $2,850 (Total) |

| Monthly Cash Flow Savings | -- | -- | $700+ Saved/Month |

The Refinancing Process with a Burlington Mortgage Broker

Navigating the refinancing process requires expert guidance to avoid unnecessary penalties and ensure you are getting the best product for your needs. Unlike the rigid structure of big banks, working with a broker offers flexibility and access to over 40 lenders. At TLC Mortgage Group, we simplify the process:

- Assessment: We review your current mortgage terms, penalty for breaking the mortgage (if applicable), and your credit profile.

- Appraisal: To access equity, we must determine the current market value of your home in Burlington.

- Approval: I shop the market to find the best rates and terms that suit your financial strategy.

- Closing: A lawyer will handle the payout of your old mortgage and the registration of the new one.

If you are unsure whether to renew or refinance, check out our guide on mortgage renewals versus refinancing. Remember, 98% of my clients would recommend me because I prioritize speed, simplicity, and security.

Q1: What is the difference between mortgage renewal and refinancing?

Renewal happens when your term ends and you sign on for a new term with the same lender (or switch). Refinancing involves breaking your current term to change the loan amount, amortization, or rate, often to access equity.

Q2: How much equity do I need to refinance my home in Burlington?

Typically, you can refinance up to 80% of your home's appraised value. This means you must maintain at least 20% equity in the property.

Q3: Will I have to pay a penalty to refinance in 2026?

If you refinance before your mortgage term is up, you may face a prepayment penalty. However, the long-term savings from a lower rate or debt consolidation often outweigh this cost.

Q4: Can I refinance if I have bad credit?

Yes, it is possible. As a broker, I have access to alternative lenders who specialize in helping clients with bruised credit. We can discuss credit improvement strategies as well.

Q5: How long does the refinancing process take?

Generally, the process takes between 2 to 4 weeks from application to funding, depending on how quickly the appraisal and legal paperwork are completed.

Get a Free Refinancing Assessment with Jason Woods Today