Mortgage Blog

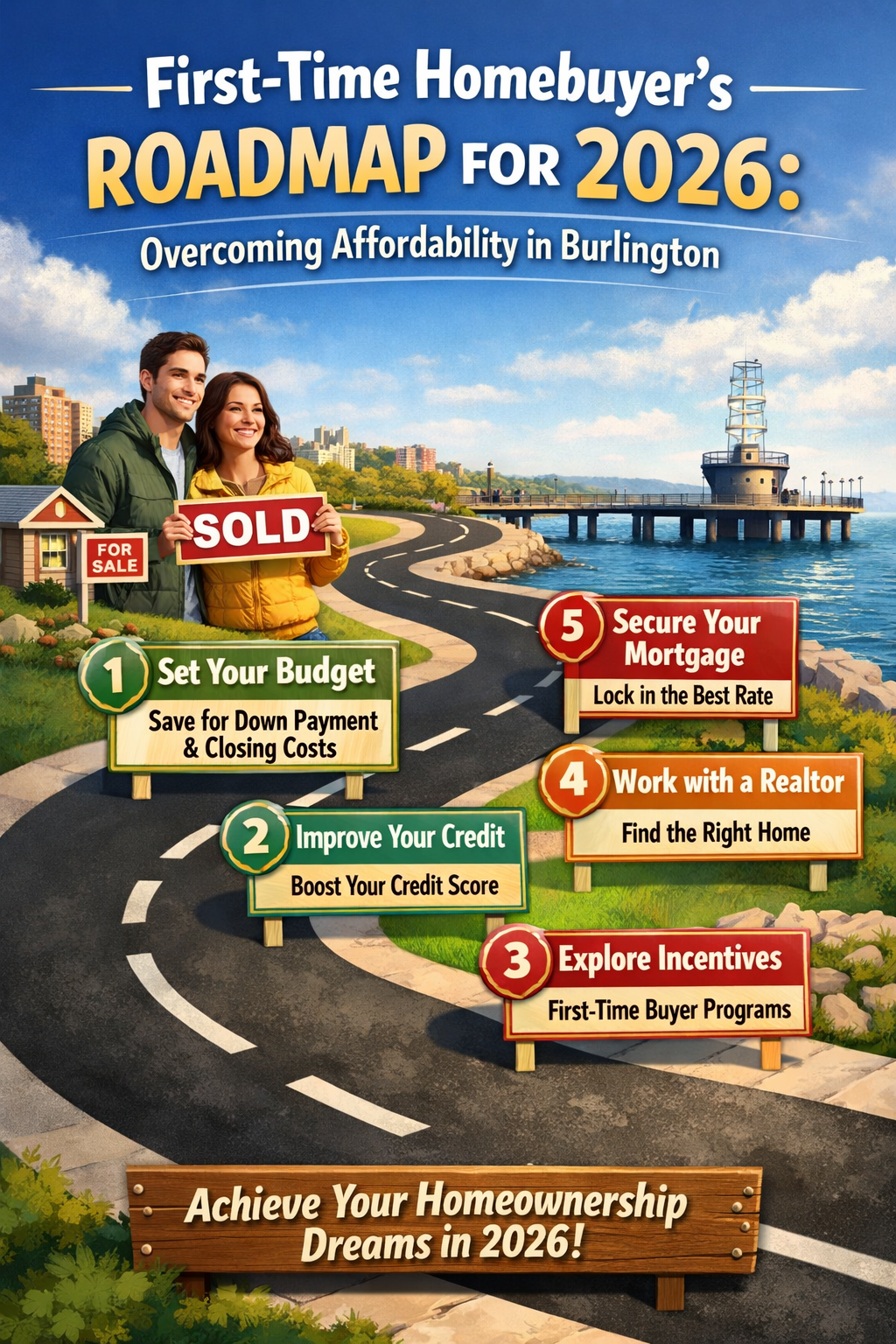

First-Time Homebuyer's Roadmap for 2026: Overcoming Affordability in Burlington

March 7, 2026 | Posted by: Matt Shepherd

Navigating the 2026 Housing Market with Confidence

Entering the real estate market as a first-time buyer in 2026 presents a unique set of challenges and opportunities. While affordability remains a primary concern for many residents in Burlington, ON, and the surrounding Golden Horseshoe area, the landscape is evolving with new strategies to help you succeed.

As a dedicated Mortgage Broker in Burlington, I understand that the 'wait and see' approach is no longer viable for everyone. Whether you are looking at condos near the Burlington waterfront or townhomes in the family-friendly neighborhoods of Alton Village, having a strategic roadmap is essential. This guide will walk you through leveraging assistance programs and smart financing to turn your homeownership dream into a reality this year.

Key Government Assistance Programs for 2026

To combat rising entry costs, maximizing government incentives is non-negotiable. In 2026, the First-Home Savings Account (FHSA) continues to be a game-changer, allowing tax-free contributions and withdrawals for your down payment. Combining this with the Home Buyers' Plan (HBP), which allows you to borrow from your RRSP, can significantly boost your buying power.

-

FHSA: Contribute up to $8,000 annually (lifetime limit of $40,000) tax-free.

-

HBP: Withdraw funds from your RRSP without immediate tax penalties to bolster your down payment.

-

Land Transfer Tax Rebates: First-time buyers in Ontario may be eligible for a rebate of up to $4,000, significantly easing closing costs.

Navigating these programs can be complex. Consulting with a specialized mortgage professional ensures you aren't leaving free money on the table.

| Scenario | Monthly Cost (Avg Est.) | Equity Built (5 Yrs) | Asset Appreciation Potential |

|---|---|---|---|

| Renting (2-Bed Condo) | $2,900 | $0 | $0 |

| Buying (Smart Financing) | $3,450 | $65,000+ | 3–5% Annual Growth |

Smart Financing: Beyond the Interest Rate

Many first-time buyers fixate solely on the interest rate, but the structure of your mortgage is equally important. In a fluctuating economic environment, choosing between a fixed and variable rate requires analyzing your risk tolerance and long-term goals.

Furthermore, getting a solid pre-approval is critical. Unlike a simple pre-qualification, a pre-approval from Jason Woods involves a thorough review of your finances, giving you the negotiating power of a cash buyer when you find that perfect home in Burlington. We also explore options like:

-

Extended Amortizations: To lower monthly payments and improve cash flow.

-

Co-signing options: Leveraging family support to qualify for a higher purchase price.

-

Purchase Plus Improvement: Financing renovations into your mortgage to buy a 'fixer-upper' at a lower price point and build instant equity.

Q1: What is the minimum down payment required in 2026?

Generally, it is 5% for the first $500,000 of the purchase price, and 10% for any portion above $500,000 up to $1 million.

Q2: Can I use the FHSA and HBP together?

Yes, you can combine funds from both the First-Home Savings Account and the Home Buyers' Plan for the same qualifying home purchase to maximize your down payment.

Q3: How does a mortgage broker help differently than a bank?

A broker like Jason Woods accesses 40+ lenders to find the best rate and terms tailored to you, whereas a bank only offers their own specific products.

Q4: Is it better to buy now or wait for rates to drop further?

Trying to time the market is risky; if you can afford the payments now, building equity sooner is often better than waiting while home prices potentially rise further.

Q5: Do I need a pre-approval before viewing homes in Burlington?

It is highly recommended. A pre-approval defines your budget and shows sellers and realtors that you are a serious, qualified buyer.